Publishing this against a deadline so apologies for any typos. I’ve been doing some thinking around how to think about current market valuations and the outlook. I’m still doing some work on the widely cited PE/10 valuation argument (spoiler, PE/10 is total garbage at this point). But I figured I’d share the analysis that kept me bullish (and invested) over the past 5 years.

The intuition was that GNP had recovered to pre-Bust levels, but employment was still well below that, so the (untapped) productive potential of the economy was much larger than it was pre-Bust.

However, I only recently got around to generating the underlying pesky-fact-based chart below (using the St. Louis Fed’s excellent FRED database). It shows Productivity – the average GNP generated by each working American since 1990 (Real GNP divided by Total Payroll Employment). The shaded grey areas are recessions.

- Recessions are generally marked with a spike in productivity. Companies lay off deadwood and frightened employees work harder to do more with less. See longer dated chart below for more history.

- However, we obviously had a HUGE spike in productivity after the Great Recession. GNP was in free fall. But employment fell further and stayed weak as GNP recovered.

- So we have had a MASSIVE leap forward in the wealth-creating potential of the economy. We are generating 7% more per worker in 2013 vs January 2008 and nearly 9% more vs January 2007.

In my view, this is the long-delayed payoff from years of technology investment. The Great Recession forced companies to make wrenching, fundamental changes to basic business processes in order to cut costs (and lay off workers). But technology enabled most of those changes. The associated pain explains why those gains weren’t realized before – we needed a Great Recession to force them through.

Productivity growth is the ONLY source of across-the-board wealth creation in the economy (otherwise one person’s gain is just someone else’s loss). So why aren’t we out in the streets celebrating our good fortune?

We haven’t found a use for the workers displaced by this productivity boom. If we could magically get those unemployed people producing at current GNP per worker, we would have a huge spike in growth. But so far we haven’t put them to work

- It has become fashionable to argue that we are facing a “permanent” structural unemployment problem. This line of reasoning has percolated far enough to reach NPR talk radio and popular magazine covers, pretty much the gold standard for conventional wisdom that is soon to be overturned. This is not the first time these arguments have been made and their popularity is usually a reliable indicator of a major employment boom ahead.

- In all reality, a LOT of those displaced workers will NEVER get as good a job as they had before the bust. They are the buggy whip makers and hand-loom operators of this particular industrial revolution. The only (cold) comfort they can draw from the whole miserable experience is that their kids will be better off. And that the House Republican’s haven’t managed to cut off Food Stamps (yet).

- But on a macro level, we will find new, productive, ways to put people to work again. We always have and we always will.

None of the productivity gains have translated into higher income per worker. I am not going to bother digging up (pesky) facts on income inequality here. If you don’t accept the inequality has become a major concern then you either deluded or stupid… or both. Please stop reading and go find a village in need of an Idiot.

- We have seen a huge expansion of wealth (S&P 500 at 1,700 – whoo hoo I am thrilled!). And the top 1% have done very well in the last few years.

- But the average Joe has seen incomes stagnate while (mild, sputtering, but still real) inflation has eaten away at the real value of those incomes.

The pendulum will eventually turn, however, as the “reserve Army of the Unemployed” is slowly re-absorbed into the economy. That is one of Marx’s best turns of phrase IMHO. In general, Marx actually had some useful things to say about times like these (he did write during the last industrial Revolution).

It remains to be seen how income inequality is brought back into line.

- My hope would be enlightened self-interest on the part of the elites (cue guffaws here). The fact that Mitt Romney was actually considered a viable Presidential candidate and that Larry Summers was considered a viable Fed Chair suggests that isn’t going to happen. I consider the Republicans more culpable (they are the Plutocratic party after all), but the Democrats ain’t much better in this regard.

- My expectation is that we will see some pretty confiscatory taxation policies somewhere down the road. I am not thrilled about this, but it seems like a reasonable bet. The fact that the idea of “confiscatory tax policy” seems laughable to most people right now is a very good sign that the pendulum has swung about as far as it can in the direction of plutocracy. We should be gearing up for an eventual (and increasingly visible) swing back towards populism. But that is another blog post for another time.

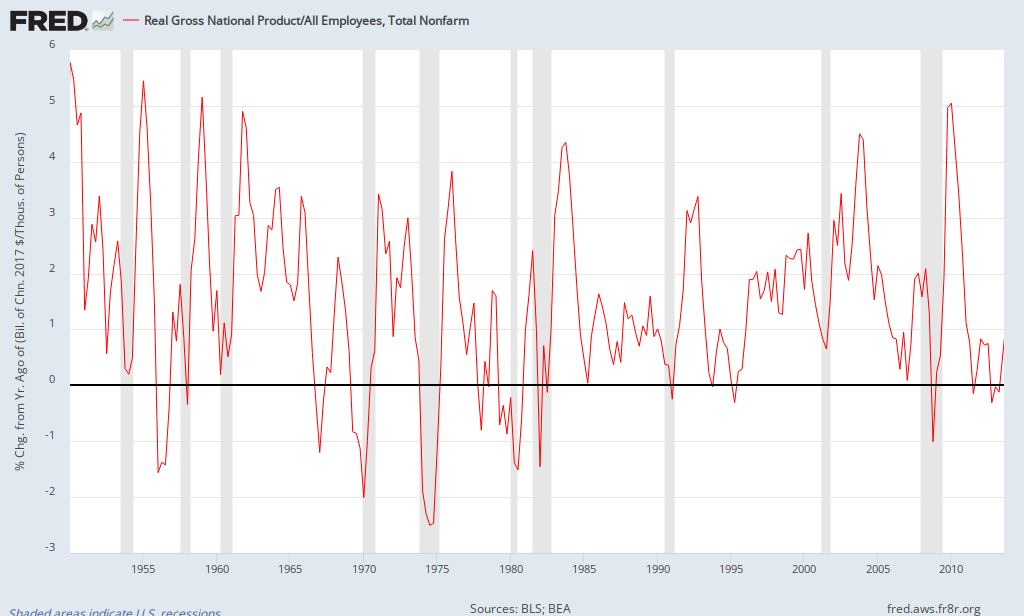

The chart below is the YoY change of Real GNP Per Worker since 1950. If you eyeball it, you can see a pretty reliable pattern of huge post-recession spikes that tail off until about mid-way though until the next recession. Hopefully we are (finally) on the verge of a similar tailing off now. Recent unemployment claims data is encouraging in this regard.

The chart below is GNP per worker since 1950 on a natural log scale. We have to go back to 1980 for a similar productivity boom. Hopefully the foretells stock market performance on par with the post-1980 boom (yoiks!?! – did I just say that?). I am told that natural logs show changes in data series over time in proportional scale. Personally I don’t really trust the slippery things (mostly because I don’t understand them). But log scales always seemed to inspire analytic confidence so I figured I’d give it a go…

2 Responses to The Market is Celebrating a Productivity Revolution. We’re Too Busy Mourning It to Notice…