So Reinhardt and Rogoff are back trying to regain their credibility (after their widely cited paper on debt levels got shredded for indefensible math errors). I learned of it from a piece forwarded by a good friend and am shamelessly ripping from our resultant exchange for this post.

R&R set up a strawman, knocked it over, and declared victory. Hurrah! But the strawman is a particularly thin one. The abstract summarized: “Even after one of the most severe multi-year crisis on record in the advanced economies, the received wisdom in policy circles clings to the notion that high-income countries are completely different from their emerging market counterparts…. predicated on the assumption that debt sustainability can be achieved through a mix of austerity, forbearance and growth… do not need to resort to the standard toolkit of emerging markets, including debt restructurings and conversions, higher inflation, capital controls and other forms of financial repression.”

R&R are weirdly ignoring what “advanced economy” policy makers are OBVIOUSLY AND ACTUALLY trying to do. Stoke inflation. This is explicit in Japan. It is highly implicit in the US. Only Europe is a mixed case. Even there, inflation is gaining favor as the preferred solution (listen to Draghi, not the Germans).

I see no sign that policy makers are trying to avoid the “standard toolkit.” Actually, they have already selected a tool (inflation) and are trying to put it to work. Either R&R (and a lot of other commentators) are dumb enough to actually believe the verbal window-dressing of the central banks. Or they are in denial. Or they are still trying to stoke the fears of default for their underlying political agendas. I think the last is the most likely explanation.

Back in the real world, it seems obvious we are facing higher taxes and higher inflation. Both burdens will fall most heavily on the wealthy. This looks like a done deal, R&R’s presumptions notwithstanding. We are probably facing a return to tax and inflation rates not seen since the ancient Clinton era. The horror! Income inequality trends of the last few decades might lead us to judge this as just a new arc of the pendulum after a VERY long swing in favor of wealth. But this would further wound the victims’ apparently limitless capacity for self-absorbed self-pity.

- We can pause here for a moment of silence for the poor, helpless victims of this “financial repression.” Cue images of jackbooted thugs standing over a cowed mass of pin-stripers. Or at least as much mass as you can gather together with 1%-2% of the population (myself probably included).

R&R, and others, seem unwilling to address this head on. Or they reflexively assume that this regime “must” stifle growth. Which leads to a forecast of stagnation. I think that forecast is likely wrong.

It is possible that growth is permanently depressed. It is more likely that we can get some decent short/medium-term growth if we can get a return of demand. That means putting people back to work.

But demand stimulation also means skewing the income equation back toward people who tend to spend most of their incomes vs people who tend to invest large portions of it. If that is “financial repression” then so be it, but there will be very few people at the barricades protesting it. The rest of the country will be at the mall.

So I guess my real point is…

- DUH! Of course we will have inflation. Or at least central banks will try their damndest to create it. And they will probably succeed. Which means we won’t have a default or any of the other awful things predicted in the paper.

- Things go in cycles. We just went through a period that has been extremely good to wealth holders. We are likely going into a period that will be a lot less friendly. That is a bummer for wealth holders, but it hardly the stuff of crisis.

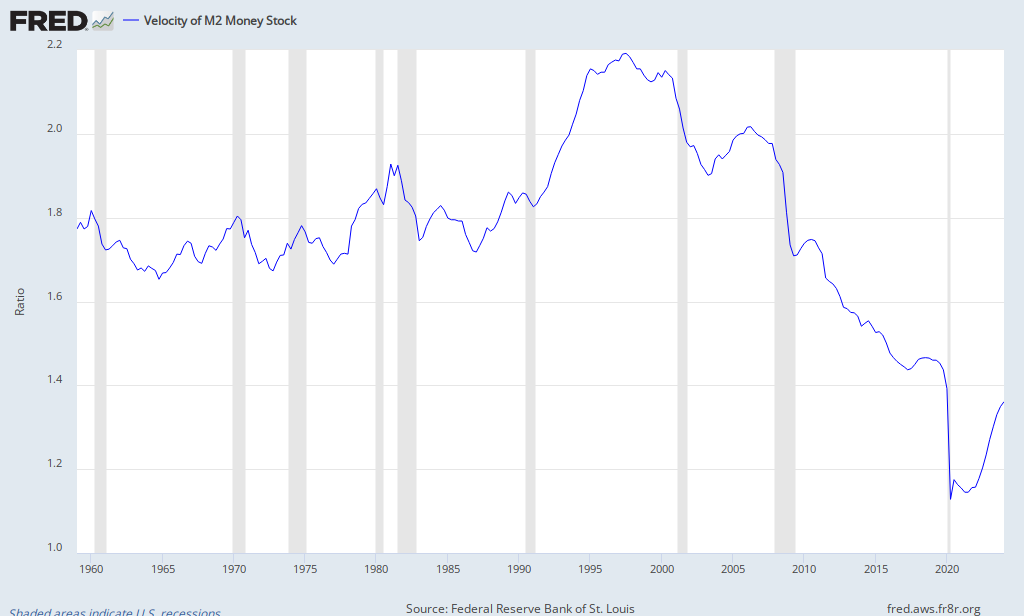

- A crisis for wealth holders is NOT necessarily a recipe for stagnation. It is likely the opposite. A shift of incomes to people with a higher propensity to spend is exactly what the economy needs. Look at the monetary velocity graph below. We need to get money circulating faster again. Not squirreling it away and then wondering why so little comes back around on the next pass of the hat.

- Inflation will also help velocity directly by forcing wealth holders to spend faster. We face a glut of savings and a dearth of demand. Putting a finger on the scale in favor of immediate consumption via inflation will do a good bit toward rectifying that.

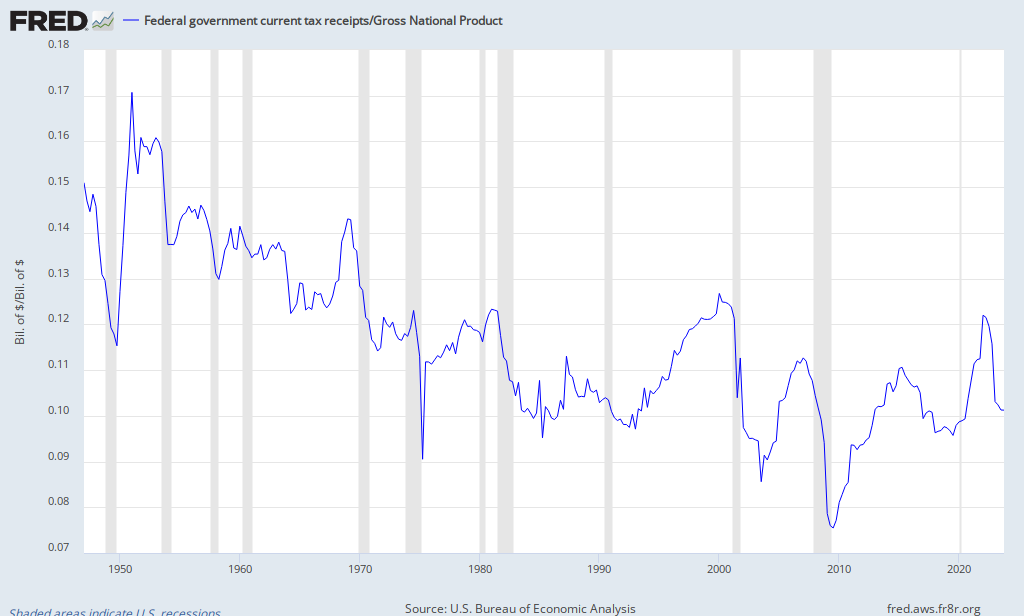

- Likewise, taxes can go up without choking off demand – provided those taxes fall on the wealthy. And provided the money is re-circulated back to someone with a higher propensity to spend it. Tax rates can’t go up forever, but see chart 2 below.

The chart the mooted victims of financial repression don’t want to acknowledge. Federal Tax Receipts as a % of GNP. This cycle has likely bottomed and has a long way to go before it starts to really crimp growth.