Pelosi is on the verge of a stunning victory. She has set a 48 hour deadline for a stimulus package “before the election.” Trump has signaled openness to a package larger that $1.8 Billion. She could find herself sending a close-to-$2 billion deal to the Senate. With language she largely dictated.

But the victory comes after that. Watching the Republican party tear itself apart with just weeks to go before the election. Putting McConnell in a lose-lose position. Either he…

…passes the bill with mostly Democratic votes. Probably after conceding even more to Chuck Schumer along the way (who can and will push for more concessions that will just peel away more Republican votes). Sparking a howl of protest from “no compromise” Republican base voters. RINO! Depressing Republican voter turnout.

…sticks with his caucus and votes the bill down. Making the Party look like the heartless jerks they are. Sparking a wave of anger that boosts Democratic turnout.

Even better (for Nancy), a desperate Trump is on the verge of committing his fading clout to getting the bill passed. Either he passes a “betrayal” bill or he fails. Either way, Trump ends up looking like a loser to base voters that value “winning” over common sense.

It is brilliant politics. It probably doesn’t, however, lead to any checks going out.

Out in the markets, we remain in a race between a darkening economic reality and levitating investor optimism. I’ve been wildly wrong about the sustainability of that optimism. However, given the continuing uncertainty of the next 6 -12 months, I remain confident there isn’t much more to it beyond good feelings We don’t know enough to know more. That is the difference between “uncertainty” and “risk.” So, absent hard facts, we are left with emotion and narrative.

The market narrative could continue to “look through” the immediate negatives. It might decide to stop looking ahead and look down. My crystal ball has been pretty crap lately so I have no idea. But if it happens. I don’t think a narrative shift will be a gentle one.

Posted inUncategorized|Comments Off on Pelosi’s 48 Hour Stimulus Deadline – Rounding Out The Circular Firing Squad?

Markets are a-twitter about the fact that Pelosi is back to talking to Mnuchin about a stimulus plan. I’d still be it ends with no deal. So why are we seeing this latest and probably final round of drama? It is most plausibly explained as masterful political theater from Pelosi.

Pelosi waited for McConnel to pass his $500b headline, $300b actual size plan in September. Ensuring she gets the last word legislatively before the calendar runs out. Meaning gets she credit for “trying to compromise” with a headline $2.4T bill. Leaving the blame gets divvied up between McConnell and the White House. If she really gets lucky, Trump tries to bully Senate Republicans into passing something and it becomes a circular firing squad. But that’s bonus points on a game she’s already won.

One way or another, no checks are likely to go out. Why?

Pelosi has actually conceded nothing in her latest offer. It is still a shit sandwich (from a Republican perspective).

Pelosi and Mnuchin are still miles apart.

Mnuchin probably can’t “deliver” Trump

None of the above really matters anyway because neither Mnuchin or Trump can “deliver” the Republican Senate, which means this is all just kabuki theater. Mitch McConnell doesn’t have the votes for much beyond the $300B price tag of his September PR exercise stimulus bill. Pelosi knows that and Mnuchin does too. Nor will he get his “line in the sand” liability protections for business. I also don’t believe a wounded Trump can whip Rand Paul, Ted Cruz, Tom Cotton, and Josh Hawley et al in line no matter how much he tweets.

Pelosi Hasn’t Offered Any Real Concessions. Mnuchin has nothing new to offer. Mnuchin Cant Deliver Trump.

3/4 of a shit sandwich is still a shit sandwich. Pelosi’s did put forth a $2.4 trillion “compromise” versus her prior $3.4 trillion plan. But from the few details I’ve seen, she offered no compromise in the specifics or spending priorities. She is offering the same (high) spending levels for fewer months (until shortly after the seating of the next Congress). So she is just cutting off a $1 trillion slice of the same shit sandwich.

Mnuchin has nothing new to offer: Per CNBC, he is still talking about the same $1.5 billion “compromise” number that he floated in August. Pelosi rejected it then. Why would she take that same deal now? Especially in light of the above – she hasn’t climbed down on any of her priorities.

Pelosi believes (probably correctly) that Mnuchin can’t deliver Trump. After last night’s debate, you would have thought the market would have figured out that no-one can “deliver” Trump. Even Trump can’t deliver Trump. He’s a puppet of his own raging id.

If it Can’t Pass the Senate, There is No Deal. $1.5T Looks Extremely Unlikely. $2.4T is Pure Fanstasy. Pelosi Knows This. that is Why SHe’s Going to Pass a $2.4T Bill.

McConnell doesn’t have Republican votes for much more than $500b-$1T. The best he could get done in his September PR exercise was a headline $500b that lets Senators claim (later) it was only $300b (by re-appropriating $200b of un-spent Fed lending support funds from the last stimulus). Rand Paul wouldn’t even vote for that number. So how do you expect him to get to $1.5T much less $2.4T? You don’t. Instead you logically conclude a stimulus bill probably doesn’t pass.

McConnell isn’t going to pass a bill with a majority of Democratic votes a month before his re-election vote. He probably wouldn’t do that if this was 2018. But he’s definitely not doing that in October of 2020.

McConnell isn’t going to get his business legal liability protections. He drew a line in the sand on that issue back in July. Pelosi wouldn’t add that as a sweetener to the shit sandwich then and she still isn’t doing it now. So either McConnel does a a humiliating climb-down (a month before the election) or he doesn’t pass a bill. Which is more likely.

Trump can’t deliver the Senate. He’s a wounded animal fighting for his life. Senators don’t trust him to not throw them under the bus the day after the bill gets signed. And Trump is too much of a coward to stick his neck out on a deal that doesn’t look certain. He probably never really tries to push a deal and likely fails if he does. Although Pelosi would be thrilled to see him try.

I could always end up surprised. We’ll know by the end of the week. Pelosi probably just serves up her $2.4 T shit-sandwich-on-smaller-slices-of bread to be tossed back and forth between Mnuchin and McConnell and Trump. Or maybe she spins out the drama by taking one more slice off the shit sandwich, but adding no sweetener. It will remain a shit sandwich and that seems unlikely to get eaten.

FWIW, I think the above will end up being worth it if we get Biden AND (more important) a Democratic Senate. Even if the market and the economy tank. Why? Because that probably means we get sustained, massive stimulus aimed at the bottom of the income pyramid in 2021. And, as I learned to my investing pain in 2020, bottom-of-the-pyramid stimulus is extremely effective in goosing the economy during or after a crisis.

If we get Biden and a Republican Senate, McConnell will go back to his Obama era playbook. Playing to win in 2024 by slow-walking anything that might help the economy over the next 4 years. that will be a disaster for investors.

If we get Trump and a Republican Senate, we’ll get more stimulus aimed at the top of the income pyramid. As we have all learned, the bang for the buck there is tiny. The money gets saved rather than spent. That isn’t disaster for investors. It might blow another nifty bubble. But that isn’t great either.

Posted inUncategorized|Comments Off on 3/4 of a Shit Sandwich is Still a Shit Sandwich. Stimulus (Still) Looks Unlikely.

Everyone knows “a tsunami of Fed liquidity” been driving markets upwards since March. So why do I keep asserting the Fed’s recent stimulus had little real-world effect (ignoring a powerful placebo effect? (see post here) Because that Liquidity Tsunami is wholly absent from the Fed’s Balance Sheet. There is just no math-based support for the “liquidity” narrative. All that leaves is the placebo effect. Powerful as long as everyone believes in it. That is the real danger of the “liquidity” narrative. It rests on magical thinking, not hard dollars.

Stick with me for a few paragraphs here. It is actually pretty simple.

The Fed has printed a huge amount of money. They doubled their asset base – adding $3.2 Trillion to their balance sheet in the past year. That basically created $3.2 trillion of “new” money – 16% of US GDP (~$20 trillion). Follow this link to the Fed’s balance sheet. All these numbers come from their data.

90% of the Fed’s money has never left the building. The Fed wrote checks to the US Treasury and to US Commercial banks. They deposited those checks back AT THE FED. They have just left it sitting there un-moving. No Tsunami. Just a stagnant lake.

90% of that Asset increase has ended up in two “Liability” accounts. Bank Reserves and the US Treasury. Depositing the Fed’s checks back at the Fed. Most of that money is still sitting there. It never hit the markets because it never left the building.

The banks have parked an additional $1.45 Trillion of excess reserves at the Fed (“Other deposits held by depository institutions”). Banks have not lent that money on. Instead, the Fed’s own data show they have severely tightened lending standards (some truly horrifying Fed “lending standards” charts here). Bank lending is down big (excluding the government-guaranteed PPP loans). If the banks haven’t lent it out, that money can’t have hit “the markets.”

The Treasury has parked an additional $1.4 Trillion in what amounts to the US Government’s checking account (U.S. Treasury, General Account). Meaning that money hasn’t been spent. I believe (could be wrong) that a lot of it is parked long-term to backstop various Treasury lending programs (like PPP and the so-far-unused commercial lending programs). But we definitely know that un-spent money can’t have hit “the markets.”

$265B went to new “cash” money (“Fed Bank Notes Outstanding).” That is actual cash in circulation. So its hard to see how it would be in the markets, Not a lot of people buy (or sell) stocks with cash.

This Fed chart shows the trend lines for Bank Excess Reserves, the Treasury’s General Account, and cash in circulation.

So we’ve got 90% of that Tsunami of Liquidity sitting stagnant on the Liability side of the Fed balance sheet. The Asset side shows how much money hit the markets

$109 Billion?!?

$109 Billion?!?

$109 Billion?!?

That is, in market terms, f**ing peanuts. Enough to buy maybe ~5% of Apple. About 1/4 of Tesla. Except the Fed actually spent it in the the even-larger debt markets, so its impact was even less consequential.

All the Fed’s open market interventions are listed below as of September 10th 2020. This are the TOTAL Fed purchases (in $ millions) in open, public markets (vs buying assets from banks, which is addressed above).

Net portfolio holdings of Corporate Credit Facilities LLC8

44,790

Net portfolio holdings of MS Facilities LLC (Main Street Lending Program)8

38,899

Net portfolio holdings of Municipal Liquidity Facility LLC8

16,543

Net portfolio holdings of TALF II LLC8

11,147

The Fed’s balance sheet expansion has enabled the massive fiscal stimulus we have seen – the $600 a week unemployment benefit and the PPP loan program. Those have had a big impact. But those have been direct payments into the Real Economy. You could argue (probably correctly) that some of that money found its way into markets. But the typical “wall of liquidity” narrative conjures up some powerful direct action by the Fed and assumes these payments out of the picture. Once you realize that 90% of the Fed’s money never left the building, you realize just how powerful that “real economy” stimulus has been. Stimulus that is now ending because the Republicans can’t get their act together and the Democrats aren’t interested in helping them out of the ditch they’ve dug. (see post here)

So what are people talking about when we hear of this “wave of liquidity” unleashed by the Fed? What is this magical “liquidity” anyway? It is literally magical – magical thinking. Extremely powerful, but wholly emotional in nature. Which is probably why market types prefer the precise-sounding term “liquidity.” Shying away from the Keynes’ more honest term “animal spirits.”

Even apart from the instability due to speculation, there is the instability due to the characteristic of human nature that a large proportion of our positive activities depend on spontaneous optimism rather than mathematical expectations, whether moral or hedonistic or economic. Most, probably, of our decisions to do something positive, the full consequences of which will be drawn out over many days to come, can only be taken as the result of animal spirits—a spontaneous urge to action rather than inaction, and not as the outcome of a weighted average of quantitative benefits multiplied by quantitative probabilities.[1]

More in my next post.

Posted inUncategorized|Comments Off on 90% of The Fed’s “Stimulus” Never Left the Building. $109B Did Hit Markets Directly. That is More Ripple Than Tsunami.

We’re in no danger of fire, but we are trapped in the house with the air filter going full blast. If you want to understand how bad it is, take a look at this air quality map (with smoke plumes enabled) from the EPA. Heading to clean air means driving 4+ hours over the Sierras to somewhere East of Reno?!? Smoke all the way to Michigan? This is nuts.

But what’s the connection to the economic policy? The same short-term-greedy, long-term-stupid calculus is apparent in both the wildfires and the Fed.

Averting Small Disasters Creates an Eventual Mega Disaster. Hopefully on the Next Guy’s Watch…

While climate change isn’t helping the fires, the immediate problem is the bill coming due for 100 years of fire suppression.

Instead of letting fires burn (frequent small, relatively manageable wildfires), we kept putting them out. Ever-more heroic, telegenic pushes. Water tankers and helicopters. Applause all round after disaster has been averted.

The dry tinder builds up.

Eventually, you get huge, destructive, mega fires.

The above is obvious and well documented. We also have an obvious and well documented solution. Prescribed burns. See this excellent New Yorker article for an in-depth look at the whys (and why-nots-even-if-its-stupid) of fire management. Or this Guardian article.

But we reliably choose to increase our long-term risk of disaster to avoid taking a short-term risk of (smaller) immediate loss. Why do we do that? Partly because we are humans. Our brains are wired to overweight the short-term over the long term.

Partly because no executive wants to be responsible for a disaster (e.g. a burn going out of control). Let the next guy take the hit. Because our brains are definitely wired to pass the buck if we can.

Dumping Money On Every Financial Market Fire Also Risks an Eventual Mega Disaster. Possibly Not on the Next Guy’s Watch…

The Fed has been doing the financial equivalent since the mid 90’s. Heroic helicopter drops of money every time the market catches fire. Money that never quite goes into “real economy” circulation or gets mopped up. As evidenced by massive increases in money supply with concurrent massive declines in monetary velocity (see post here).

As with forest fires, the problem is that you never know when a whole pile of cash is finally going to go up in smoke. It might have been the 2008 Financial crisis. It wasn’t. It might (still) be the 2020 pandemic. We might also get by. I have no better idea than the next guy, even if I were sitting next to Chairman Powell.

But We Do Know There is a Lot of Dry Tinder Out There.

We also know the conflagration would be pretty ugly if it gets going. The risks (and eventual damage) go up with every “successful” intervention. Especially as the boomers don’t have the time to dig themselves out of a financial hole before they retire. If their asset values go down (and stay down), we will end up carrying a lot of impoverished old folks for a very long time. Old people who have the time to vote.

The above is why I remain cautious. I don’t think know better. Lord knows I’ve been super duper wrong for the past 6 months.

But we all know there is a lot of dry tinder out there. At some point, it starts to make sense to pack up the car and evacuate at the first whiff of smoke. Even if your end up looking foolish. I’d also note that, in a financial sense, too many people packing up the car and evacuating is also known as a “market crash.”

We are also hardly out of the (dry, tinder-filled) woods. I still look ahead and (still) seeing more uncomfortable “uncertainties” than manageable “risks.” FYI, In the language of Economics. there is a bright line definitional difference between the two words:

risk is present when future events occur with measurable probability

uncertainty is present when the likelihood of future events is indefinite or incalculable

Rather than ranting on, I’ll link to this excellent FT article as a summary of the negatives. I have no idea if he is right. He has no idea either. That is sort’ve the point. We have a lot of “uncertainties” over the next 6-12 months and a lot of dry tinder about …

FYI Monetary Velocity Has Crashed Since March. Follow Link Chart Doesn’t Display.

The news keeps running ahead of this post! Mitch McConnell has confirmed a new stimulus package isn’t likely (see full explanatory quote at the bottom of this post). Read on for how and why we got here…

Absent new stimulus, we are likely headed off a cliff. While the Fed got the headlines, the $600 a week unemployment benefit and PPP did most of the heavy lifting keeping the economy from going off a cliff. A view supported by the Fed’s so-far-too-quiet begging Congress for a new stimulus package (see related post here).

Whether we land with a bump or a crash, cliffs are bad and usually avoidable. That will down-trend the economy and (likely) financial markets going into November. With real potential for a serious downward spiral, especially in more reactive (really bi-polar these days) financial markets. Especially with virus case counts likely trending up.

So how and why did we come to this pass?

Pelosi Set Up a Lose-Lose Situation for the Republicans

Pelosi has been running this show since summer. She set a ludicrously high bar at $3 Trillion, then “compromised” down to a (vaguely defined) $2 Trillion. She has refused to budge since. Leaving the Republicans with two choices.

Climb down and accept her “compromise” number. Humiliating them in front of their base voters with a few months to go until the election.

Refuse and spend nothing at all. Sending markets and the economy into a down-trend at least and potentially a downward spiral. With a few months to go until an election.

It looks like we’re heading down the more destructive path #2. Less because the Republicans made an active choice and more because they never got their act together. No cohesion in the Senate. No trust Trump would give Congressional Republicans air cover on any compromise deal. Lacking internal cohesion, they have never put a serious counter-proposal on the table.

McConnell will pass a face-saving $500B-$700B bill in the Senate (see below), but that is going nowhere. They know that. As the “party in power,” most voters will mostly blame the Republicans. They know that too. So how did the Republicans set up this trap for themselves? And why did Pelosi decide to spring it now?

The “Madman Strategy” Works Great Until Someone Calls Your Bluff.

Over the last 30 years, the Republicans have leaned harder and harder on the classic “Madman Strategy” in negotiations. Playing a game of chicken with the Democrats. Betting the Democrats will bail out first.

Hold up some urgent, necessary action (like raising the debt ceiling) with a maximalist, no compromise stance that plays well with the base.

Wait for the Democrats to “act reasonably” at the last minute to defuse the situation.

Teeing up another round of base-pleasing via a sneering, hooting victory dance over the weak, compromising Democrats.

In the eyes of their base, they have made “compromise” into a Democratic vice and un-compromising intransigence (the madman strategy) into a Republican virtue.

That has left their base with deeply unrealistic expectations. The base doesn’t expect just wins, they expect domination. Own the libtards! Compromise is for the other side! For wimps! For the effete, vaguely European, urban elite Democrats! Manly, red-blooded, American Republicans know these colors don’t run!

Reliably Threatening to Drive the Car Off The Cliff is Reliably a Bad Idea

Over-reliance on that madman strategy has left Republicans at the mercy of Democrats. In a game of chicken, the Republican base expects them to drive the car off the cliff rather than stand down. That pays off in admiration and donations, but one of these days you’re still going to go flying off a cliff. The other guy gets to decide when.

Your opponent will call your bluff when the self-damage will be greatest, their gains will be worth it, and the blow-back damage to them is mostly manageable. That seems like a pretty apt description of this moment in time and Pelosi’s view of it.

The “madman” is pre-commited to do something stupid and self-harming. He is relying on the other party to save everyone from his folly. One day, they won’t climb down. They will force you to either 1; climb down, or 2; follow through on a “mad,” self-destructive threat.

The “madman” threat here was to tank the economy and hurt millions of out-of-work American voters. Leaving Republicans dependent on Pelosi letting them claim a “win.” Less as a matter of policy and more as a matter of perception. It had to look like Pelosi backed down.

If Pelosi didn’t climb down, the Republicans were pre-commited to one of two losing options. 1; If they climb down, they lose. 2; If they drive the car off a cliff, they lose. Moreover, the Republicans gave Pelosi the ability to force them into those losing choices.

Nancy Pelosi Decided to Call the Republicans Bluff On Further Stimulus.

Pelosi is dangling a rope cut deliberately too short for the Republicans to grasp it. This has been increasingly clear for months. She’s never been interested in a compromise deal. She’s only interested in looking like she’s seeking a compromise (to avoid blame). Her timing looks pretty good, with 2 months to go until a pivotal election.

If the Republicans had climbed down and compromised, they would have looked like wimps. Pelosi would have made that clear with a victory dance loud enough to show up on Fox News. Wimps don’t get the base to turn out in 2020. Wimps get primary challenges in 2022 and 2024 from wackadoodles promising even-greater-intransigence. Republican Senators who aren’t up for re-election in 2020 know that vote would be an albatross around their necks forever. They also know Trump will throw them under the bus on a deal that plays badly with the base.

How steep a cliff and how soon will we hit the ground? I think it will be bad (eventually) for the economy and worse (quickly) for markets. Meaning the market reaction comes before the November elections, but the economic damage compounds slowly over months. Although I’ve been totally wrong on the market for the last 6 months so…

Who gets the blame – or the smaller allocation of it? There will be blame all around, but I’m guessing more of it will stick to the Republicans. Voters will apportion most of the blame to the presumed madmen – Trump and the Republicans. The Democrats, assumed to be the party of compromise, will probably escape most of the blame. Usually the White House incumbent gets blamed for bad stuff. The public expects the Democrats to find a compromise.

Pelosi knows all of the above. She took the logical path to maximum gain. Play this game of chicken to the end. Forcing the Republicans to either climb down or drive us all off a cliff. She wins either way. Provided Pelosi keeps up the “compromise theater” act, she probably gets away blameless for with what is, in fact, a madman strategy of her own.

A Deepening Crisis and Declining Market Helps Democrats Politically.

Pelosi’s political interests are better served by a bill NOT passing – threatening market optimism and exacerbating the current economic crisis. That might be bad for the nation, but it is good for her narrow, short-term political agenda.

With the key caveat that she can pin most of the blame on the other party. Where she is doing a decent job if not brilliant. Good enough to avoid most of the blame in November. Yes we’re going off a cliff, but she wins the election. And the damage looks manageable given a new (presumably Democratic) Congress in 2021

Markets Move Fast and a Crash Helps Pelosi Most. The Economy Moves Slower. The Damage Can be Mostly Un-Done After The Democrats Gain Power.

A market crash would depress Republican turnout and boost Democratic turnout. It takes away one of Trump & Co’s last talking points. It hurts affluent Suburban Republicans most. They will mostly blame their own team. Affluent Democratic voters will also take a hit, but that hit is more likely to energize them to turn out and vote (against Trump). The tiny remainder of “swing” voters left will also shift against Trump & Co.

The economy is also struggling, but it is a slower-moving beast. Damage done in October 2020 can be (partially) un-done in February 2021. Especially if the new Congress has a Democratic majority to pass bottoms-up stimulus bills in the House (assured) and the Senate (less assured). That logic holds even if Trump remains in the White House BTW. The Senate is more important than the Presidency.

In 2021, credible moves to revive the economy would probably also revive the markets. Wall Street may lean Republican, but a Democratic President and Congress are more likely to direct stimulus where it has proven most effective – at the bottom of the pyramid. The Fed is nearly begging for more fiscal stimulus to veer the economy away from deflation. The market is likely to respond well to fiscal taps opened wider and targeted more efficiently. Poor people spend. Rich people save. We need more spending and less saving.

But, even if a crash and downturn cause permanent damage, Pelosi gets what she wants. That may be all that matters. She’s the Democratic Speaker of the House, not Mother Theresa.

The above is why I stopped expecting a new stimulus package back in July. Pelosi’s actions suggested she was going to call the Republicans bluff. Force a climb down or a drive off a cliff. She is going madman on the madmen…

Why Do People Assume Pelosi Wouldn’t Do What Mitch McConnell Clearly Would?

The above is ugly, cynical, selfish politics at its worst. Exactly what we would expect Mitch McConnell to do if the tables were turned. Or Boris Johnson. Or Donald Trump. Or Putin.

But for some reason, most people seem to assume that Pelosi wouldn’t do this. Why? I think because they are so used to the “reasonable” Democrats compromising in the face of the Republican’s madman strategy. They assume the Democrats will eventually cave in and “do the right thing for the nation” in the face of Republican intransigence.

That assumption works in Pelosi’s favor here. If there is no deal, people won’t jump to the conclusion the “compromising, weak Democrats” were the responsible party. Because the Democrats are, well, “the Responsible Party.” If we go off a cliff in a game of chicken gone wrong, most people will blame the assumed maximalist madmen. Pelosi, assumed to be reasonable, can “unreasonably” force the Republicans into collective suicide.

That is pretty good politics. Given the things at stake in this election, it might even be good policy. We need more stimulus and the Democrats are more likely to deliver it. Even Wall Street will eventually figure that out.

OK. THis post has been a bear to write so I am going to stop wrestling with it and just wrap up here. I’ll leave you with a great Key & Peele clip below. The Republicans are the guy shouting “hold me back” in the face of an incipient bar fight”. I’ve also included the “Game of Chicken” scene from Rebel Without a Cause.

News Update and Commentary from Sunday’s Axios “Sneak Peek” Newsletter.

Driving the news: Nearly every morning during recess, Senate Republicans had a call with the White House’s top negotiators, Treasury Secretary Steven Mnuchin and Chief of Staff Mark Meadows, to discuss the status of the stimulus talks and where the vastly opinionated conference can find common ground.

Most GOP senators, particularly those in competitive re-election races, agree that they need to do something to cushion the economic blow of the pandemic, despite largely disagreeing on what legislation should like.

The conference has decided that they can get behind a narrow, scaled back package that addresses only the key issues with widespread GOP support, including more money for schools, widespread liability protections and restructured unemployment benefits.

“We have a focused, targeted solution that we hope the House would pass,” Sen. John Barrasso (R-Wyo.) said Tuesday.

Between the lines: Many Senate Republicans privately expect this effort will fail but see the expected vote as a maneuver to put Democrats, who passed their $3 trillion HEROES Act in May, on defense.

“They would like to change the conversation and highlight the immediate needs in a skinny bill and force Democrats to essentially shoot it down,” a Senate GOP aide told Axios.

Posted inUncategorized|Comments Off on Pelosi Called The Bluff In the Republican’s Game of Chicken. We’re Going Off The Cliff.

Right after I wrote my post saying I didn’t expect stimulus, news broke that suggests Pelosi and Mnuchin don’t see it either. So I’m noting that here. More evidence we’re headed towards a major Policy Failure (Econ speak for a shooting yourself in the foot). The markets have tanked in the two days since that news broke, although that might just be coincidence. I still think most investors and executives are blithely assuming “they will do a deal” based on the (obvious) benefit to re-election campaigns etc. That assumption stands on shakier ground every day closer to Election Day.

The news; Pelosi and Mnuchin have agreed to detach any stimulus deal from a “clean” continuing resolution to fund the government. If they thought a stimulus deal was in reach, they would have used the short-term spending bill to push it through.This strongly suggests they don’t expect to pass a stimulus soon (if ever).

Per my prior post: Looking at the big picture, passing a stimulus package seems like an obvious, logical move. But the mechanics look impossible when you work from the bottom up. Remember that nothing happens without 51 out of 100 Senate votes AND Bernie Sanders agreeing to not filibuster. Or 60 Senate votes if Bernie does filibuster.

A reported 15-20 Republican Senators weren’t willing to support McConnell’s $1 trillion trial balloon (that notably never got turned into a bill). The largest package McConnell can pass with all-Republican votes seems to be about $500b (as reported this week). The common thread seems to be Senators NOT up for re-election in 2020. They are looking at the 2008-2009 experience and fearing (rightly) that any vote for “stimulus” will become an albatross around their necks in the 2022 and 2024 Republican primary season. Or the 2024 presidential Campaign – here’s looking at you Ted Cruz.

McConnell isn’t going to get 5-10 Democratic Senators to cross the aisle and vote for a $500b package nor, probably, a $1T package. The higher the price tag goes towards $2 trillion, the more he will need to depend on Democratic votes. I just don’t think McConnell would pass a bill with a Democratic majority (e.g. 26 Democrats and 25 Republicans). If you think McConnell would do that, I’ve got a lovely bridge in Brooklyn to sell you. Especially as McConnell is also up for re-election this year.

Most reporting give Pelosi credit for “compromising down” from $3T to $2T. Pelosi’s has since stuck firm to that $2t+ number. But there is a lot less to that $1T cut than meets the eye. Last I saw specifics, her “come-down” from $3T was mostly spending the same amount (per month) for fewer months. “OK, I’m willing to cut the headline price tag by only funding the same total spend until the next Congress is seated (instead of funding it well into 2021).” Pelosi has also been (deliberately) vague about what her proposal actually entails.

So McConnell is sidelined because he can’t get a deal done. Trump’s usual approach is to wait for other people to bring him a deal (and then either take the credit or throw everyone under a bus depending on the polls). Pelosi is working very hard to look like she’s willing to compromise, but making no apparent effort to reach an actual compromise.

The equation above does not solve for a deal. It solves for a short ride off a tall cliff in a game of chicken gone bad. The Republican party are the guys with their jacket caught in the door, but we’re all likely to take a hit from it. (a classic “Rebel Without a Cause” clip below).

Pelosi’s motivation are, I think, particularly misunderstood. Pelosi’s political interests are better served by a bill NOT passing – threatening market optimism and exacerbating the current economic crisis. Going into November, a deepening crisis and a declining market likely help the Democrats politically. With the key caveat that she can pin most of the blame on the other party. That might be unequivocally bad for the nation, but it is good for her narrow, short-term political agenda.

The keystone (potentially false) assumption is that Pelosi will put the national interest over her political interests. There is no guarantee this happens. What would Mitch McConnell do if the tables were turned and Obama was President? Reading Pelosi’s actions so far, she seems to be playing this more for political gain than with an eye towards a resolution. In other words, hoisting Mitch by his own petard.

More on that tomorrow.

Posted inUncategorized|Comments Off on Pelosi and The White House Don’t Expect a Stimulus Deal Anytime Soon…

Investors seem to be assuming we can get a stimulus without a crash. It may be that we need a market crash to get a stimulus. People (and the market) are assuming additional stimulus (unemployment checks and PPP). I am far less confident. Unless you pencil in a market crash. Absent that sort of shock, inaction may rule. Part 1 is below, Part 2 to follow shortly.

The yearning for fiscal stimulus is growing out there.

It is starting to sink in that the unemployment checks and PPP handouts loans have been doing most of the heavy lifting out there in the real economy. That stimulus has worked incredibly well. Much better than I expected. A big reason why I have been so totally wrong on the market since March (I promise to write up a “lessons learned” piece eventually).

That success pains a lot of Republican-leaning investors. Why? They are desperate to avoid the obvious conclusion that future stimulus should look like that successful model. Giving money to poor people (who immediately spend it into the “real economy”) instead of squandering it on tax cuts for rich people (who squirrel it away in the “asset markets economy”).

But that is a problem for later. A market drop would pain them even more. So Wall Street is begging for stimulus. I see a lot of commentary assuming that stimulus will happen. The basic line of argument is “They have to do it if they want to be re-elected. The Republicans will hold their noses and vote for something larger than $1 trillion. The Democrats will hold their noses and vote for something smaller that $2 trillion…”

That argument is based on the collective, top-down interests of the Parties. It makes a lot of sense. But it breaks down when you look bottoms-up – counting votes in the Senate and looking at the power dynamics.

I Have Not Seen a Credible, Inside-the-Beltway, Count-the-Votes Analysis That Delivers a Stimulus Absent a Catalyst (Like a Crash).

The Republicans need to summon the collective will to act in their collective self interest. But their individual self interests may be pulling too hard in the direction of a collective failure.

I worry we have a situation where “the base” of neither party will forgive a compromise so close to an election. Especially the Republican base which is a more unitary force driven by rhetoric that equates compromise with weakness. Exacerbated by a President with a track record of throwing Republican Congressmen under the bus on delivery of a hard-fought, necessary “compromise” package.

15-20 Republican Senators seem to have come to the conclusion that compromise is not in their personal best interest. Republican Senators up for re-election in 2020 may be desperate to pass a bill, but their colleagues facing voters in 2022 and 2024 are thinking about how that vote will play down the road. Especially those eyeing Presidential bids (e.g. Ted Cruz**). Everyone wants a deal, but no-one wants to lose their seat for it in 2020, 2022, or 2024. With that in mind, lets set out the “known knowns” from the bottom up.

McConnell/Senate:

We know 15-20 Republican Senators (29%-38% of the 53 total), were NOT on board when McConnell floated his @$1 trillion proposal back in July. Notably, that proposal never emerged as an actual Bill. McConnell never risked an up/down vote. If reports from yesterday are correct, $500b is the largest number McConnell thinks he can actually pass next week.

It is VERY hard to see how he gets 5-10-15 Democratic Senators to cross the aisle. That is impossible with a $500m bill and unlikely with $1 trillion. As the price tag goes higher, McConnel will gain more Democratic votes, but lose more and more Republican votes. It all probably doesn’t add up to 51.

The above is why McConnell was sidelined in the July/August negotiations. He can’t deliver a majority of votes for any bill that might pass the House. At least not with a Republican majority. McConnell could pass a $2 trillion bill in a heartbeat with a majority of Democratic votes. But he’s not going to do that – especially with his own election fight to win in 2020.

So the White House’s reported $1.3 trillion number probably can’t pass the Senate without heavy lifting by Trump. Active, loud, unequivocal support. Air cover, pressure, and veiled threats for those wavering Republicans to (hopefully) push through and sanction the compromise deal.

If Bernie filibusters (requiring 60 votes to over-ride), any package is probably dead in the water. Oddly this gives Bernie & Co. the final say in the process. Just like back in March when 4 Republican Senators tried to scale back the $600 unemployment benefit at the last minute.

Pelosi/House

Pelosi understands the dynamics above. That is why she isn’t negotiating with McConnell. He’s a bystander. Trump has to deliver the deal. So she’s dealing with Trump.

She has three yawning trust gaps. 1). She doesn’t trust Mark Meadows personally. 2). She doesn’t trust that Meadows or Mnuchin can deliver Trump. 3). She doesn’t trust Trump. Personality issues aside, Trump always tries to re-negotiate deals at the last second.

So Pelosi isn’t going to move until Trump moves. Whatever Meadows, Mnuchin, or even Trump promise is worthless. Action is all that matters. She will wait to see Trump tweeting in support of an actual, marked-up Senate Bill.

She can deliver the House. Or walk away. The Speaker has tremendous power. Reports of a “revolt” in her caucus are 1). Probably stage-managed to give moderate Democrats political cover. 2). Functionally irrelevant. If Pelosi doesn’t want a bill hitting the floor, it isn’t hitting the floor.

She knows Bernie can stop any bill in the Senate.

Trump/Administration

Who knows what sort of deal Trump is willing to promote? I have no idea. Meadows and Mnuchin likely don’t know either. All we know is that we don’t know. Until Trump sends out a few tweets. Even then…

We know that, rhetorically, Pelosi has done all she can to paint Trump into a corner where any deal is seen as a climb-down “compromise.”

We know that Trump hates anything that smacks of “compromise.” And he will likely refuse to accept anything that looks like a “loss.”

Could Trump spin an eventual deal as a “win?” He can try. Pelosi seems pretty intent on denying that. The day the deal gets passed, she is going to be out crowing about a “win” and “making Trump back down.” The louder she celebrates, the more it hurts Trump. Pelosi will find a way to make her celebration go viral. Fox news can drown out a lot, but an NFL-style touchdown celebration (perhaps literally?) will be pretty hard to ignore.

Just step back and ask the simpler question. Does this seem like Trump’s style? With an election coming up? Has he ever really done this before? “a huge lift by Trump. Active, loud, unequivocal support. Air cover for those wavering Republicans to (hopefully) push through and sanction the compromise deal.”

Put all the above together and a deal looks pretty unlikely. I’m inclined to take Pelosi’s stated frustration at face value. Facing the above, she is negotiating over exactly what with exactly whom? Promises made on behalf of a President who routinely breaks them? On a bill that McConnell’s Senate can’t/won’t actually pass?

This hole looks too deep and wide for Pelosi to bridge. Even if she wanted to. Her own political calculus argues for NOT enacting a stimulus – provided she avoids the blame for it. More on that in my next post.

The longer the negotiation theater goes on, the harder it is going to be for the market to ignore. Risking a market crash. A market crash that would almost certainly catalyze a new stimulus package. A pre-election market crash that also serves Pelosi’s longer-term interests.

We May Need a Crash to Get a Stimulus…

The complacent consensus response to the above tends to be a shrug. “They will eventually do a deal. They always do.” Relying on the (said-with-a-sneer) “compromising Democrats” to pull the “principled Republicans” out of a ditch.

What if Pelosi & Co don’t play along with the game? “Everyone” expects them to compromise for the long-term good of the nation. What if they stand firm and play this for short-term political gain?

Win the election and deal with the damage done in February. After the last 4 years, what would you choose?

We all know that is what Mitch McConnell would do. The longer this negotiation theater goes on, the more it looks like Pelosi is following that same playbook.

What does that imply? A much higher chance of a market crash (and incipient economic crisis) in the next 2 months. This doesn’t seem to be what is expected or priced in.

** I note Ted Cruz because he is the archetypal Republican politician of this era. Opportunistic. Focused on power. Flexible to the point of indifference on policy or even principal. Look at this situation through his eyes.

He is looking at the 2024 presidential election and his own re-election.

Voting for a “stimulus bill” threatens him in both. He doesn’t want to see “bailout Ted” or Stimulus Ted” or “RINO Ted” commercials against him from an even-more-far-right primary challenger.

What about risking the Senate majority? That’s not Ted’s problem. Ted takes care of Ted. He has his own elections to win. Its easier being the opposition anyway. No responsibility and lots more room for fantasy economics (tax cuts create growth!) and fantasy science (clean coal!).

Risking Trump’s wrath? In 2024, Trump’s is either running for President again (against Ted) or a lame duck. Arguably Cruz wants Trump to lose. Its going to be a lot easier to run “against” Biden instead of “for” another 4 years of Trumpism. That also gives Cruz et al 4 years to try and pry the party away from Trump and his dreams of a family dynasty. For our sake I hope they succeed.

Posted inUncategorized|Comments Off on Stimulus Looks Pretty Unlikely. Unless You Pencil in a Market Crash First…

The Fed has always been seen as Republican-leaning player in politics. After all, the Fed’s main job is to look after the best interests of regulate the banks. But it occurred to me that, right here and now, Powell has a lot of good reasons to favor a Democratic Presidential and (more crucially) Senate win.

(Near Term): The Fed Desperately Needs More/Continued Fiscal Stimulus.

The Fed’s only real tool is to flood the banking system with money. That is all for nought if the banks don’t lend it onwards. Instead banks are (very reasonably) tightening lending standards. So that money isn’t finding its way into the economy.

The main props for the economy over the last few months were the PPP business loans and the $600 unemployment benefit. Those aren’t being renewed. Why? It ain’t Trump. His objections are a sideshow to the real problem. 15-20 Republican senators that won’t vote for any new money for anyone – all with an eye towards their 2024/2022 elections.

That voting block isn’t going to budge. Leaving the Fed holding the bag and the blame if the pandemic knocks down a debt-fueled economy’s house of cards. Unless the house of cards falls before November. The election takes place in the midst of a crash. Blamed on Congressional inaction. Those 15-20 Republican Senators end up in the minority.

(Medium Term). The Fed Desperately Needs MORE Inflation.

The Fed is practically begging (in very polite Fed speak) for more fiscal stimulus. Partly to sustain the economy short-term. But also because they desperately need to kindle some inflation. Everyone at the Fed knows deflation is a killer for banks. They also know that inflation is a whole lot easier to fight at some future date. Deflation is a bitch to kill once it sets in (see “Japan”). The best route to inflation is through loosening the governmental spending taps. Particularly working from the bottom up.

The $600 unemployment benefit has demonstrated this unequivocally. That money has been spent fast and almost entirely into the “real” economy. By contrast, the Fed’s increasingly ineffectual money-printing since 2008 has ended up parked in various asset markets without ever circulating into the real economy (cue declining monetary velocity).

Side Note: The relative effectiveness of that $600 is exactly why Republicans hate it so much.It shreds 30 years of ideological flim flam economics. The most effective response to a major downturn is to hand money to the people most likely to spend it immediately? Who would have ever guessed such a thing!?!

The anti-inflation narrative has always been “don’t let those bolshie left-wing politicians get their hands on the spending taps! They’ll end up raising the long-dead monster of inflation!!!!” With the monster of deflation at least halfway out of the grave, maybe those left wing spendthrifts are exactly what we need. To extend the Japan metaphor, maybe we need an inflationary Godzilla to fight back a deflationary Mothra. The battle might wreck a few buildings in Tokyo, but it is better than just Mothra unchecked.

(Long Term). The Fed Desperately Needs Adults in Congress (and Wall Street).

Every Central Bank in the world is sick of pulling politicians out of ditches they keep driving into. Politicians have grown equally comfortable driving into ditches, knowing the Central Bank will always come do the heavy lifting to pull them out. Daddy will just dust me off, get me a new car, and I’m back on the road.

Investors have grown equally as comfortable. The Fed will always step in to stop a crash, but they never tighten rates if the market revolts. The current rally boils down to a simple continuation of that faith. “Don’t fight the Fed” is just another way of saying “The Fed will always save us, so pile on the risk….”

Everyone knows this. Central Bankers most of all. They have always stepped back from the ultimate solution. Let a crisis inflict real losses on politicians and investors alike. The timing has always been tough. Like St Augustine “Oh, Master, make me chaste and celibate – but not yet!”

The current crisis (created by failure to re-up the $600 payments and PPP) presents particularly fortunate timing for a crisis. It comes in front a major US election. A massive wipe-out for over-their-skis investors and posturing politicians would do wonders to drive home a lesson that Daddy isn’t always going to come save you. Engineer a serious crash where the most feckless drivers take a permanent, painful hit.

That sets up a few months of serious turmoil and pain, but it also sets up a new Administration and Senate in February. Precipitating that crisis is potentially a risk worth taking for the Fed. Especially as we now know just how rapidly and effectively a relatively tiny $600 weekly stimulus makes its way into the real economy when targeted at high-marginal-propensity-to-spend individuals (generally known as “poor people”). Even more so if that new Administration tees up other inflation-kindling measures that help the Fed steer its flock of banks away from a deflationary abyss.

Most importantly, the Fed would finally kill the “moral hazard” trade for politicians and investors alike. As someone once observed, air bags aren’t the “best” way to reduce auto accident injuries. Mandate instead that driver-facing, needle sharp spikes get mounted on every steering wheel. The prospect of being impaled would do wonders to ensure good driving behavior. An October crisis re-creates that awareness of risk and permanent loss, with a decent shot at a reasonable recovery effort starting 3-4 months later.

Would the Fed Actually Do This? Probably Not.

The above all seems a little far-fetched. Does the Fed have the means to precipitate a crisis? Almost certainly yes. Probably just by standing aside. Failing to ride to the rescue as cash flow starvation drags down the real economy. Is the Fed really that political? Maybe, but I hope not). Do they have the courage to pull the plug like that? Probably not.

However, Powell just might decide he has no choice. Look at his alternatives. If Biden wins, he faces the prospect of carrying the burden and the blame over 4 years after Mitch McConnell goes back to his Obama-era posturing against any of Biden’s spending plans “because we can’t possibly afford it (after all those tax cuts).” If Trump wins, he faces the the even-more-horrific prospect of him appointing more wackadoodle gold bugs like Judy Shelton to the Fed’s Board.

The fortuitous election timing also points towards taking (in)action. Eliminating the one-way risk trade would restore a lot of power to a Fed rapidly running out of real-world policy levers to pull (vs placebo effect PR moves). They know they are on thin ice, at the zero-lower-bound, and already at negative real rates. And they know how much its sucked to be the Central Bank of Japan the last few decades. Maybe this is the time to make a stand?

Heck, a “good crisis” now also might just save us from future deflation. I don’t want to get my hopes up, but that would be a price worth paying.

FYI I’m back at home in front of a real keyboard (hopefully meaning fewer typos). RV trip back across country was a lot of fun actually. Lots of adventure and surprisingly little drama. I need to do a “what did I get wrong?” piece one of these days. But the thought above struck me so figured I’d share. OK, baby’s crying so hitting “send.”

Posted inUncategorized|Comments Off on Does the Fed Want the Democrats to Win? Might They Act to Make that Happen? Fun With Conspiracy Theories…

I am hoping for push-back here, so please poke holes! Question my assumptions! Help me think this through!

Looking at the past 20 years, it is clear we have an increasingly fat jockey (wealth) riding a faltering horse (the real economy). This might continue for some time, but it can’t continue forever. The resolution is likely to be ugly – either via the fires of asset write-downs or the freezer rot of inflation.

If I were alone in that view, I’d doubt my own judgement or facts or both. My reading this summer has given me courage to write this post. A former head of the Bank of England sees those same imbalances (see Mervyn King’s “The Alchemy of Finance“). Two respected heavy-hitters spotlight “the” major cause of those imbalances (see “Trade Wars Are Class Wars“). So I’m not alone in seeing those imbalances or worrying about an ugly resolution. I may well be alone and wrong in the below, but here goes…

Over the last 20 years, the US has pumped a huge volume of dollars into increasingly stagnant pools of non-circulating paper wealth. The money has piled up much faster than the economy has grown. Those stagnant pools might give us a rough estimate of “the Bezzle.” Paper wealth that exists only as long as a financial confidence game lasts.

“At any given time there exists an inventory of undiscovered embezzlement [not the illegal kind. The legal, clever Wall Street kind. Think 2008’s mortgage backed bond bubble] in — or more precisely not in — the country’s businesses and banks. This inventory — it should perhaps be called the bezzle — amounts at any moment to many millions of dollars. It also varies in size with the business cycle. In good times people are relaxed, trusting, and money is plentiful. But even though money is plentiful, there are always many people who need more. Under these circumstances the rate of embezzlement grows, the rate of discovery falls off, and the bezzle increases rapidly. In depression all this is reversed. Money is watched with a narrow, suspicious eye. The man who handles it is assumed to be dishonest until he proves himself otherwise. Audits are penetrating and meticulous. Commercial morality is enormously improved. The bezzle shrinks. https://www.goodreads.com/quotes/tag/bezzle

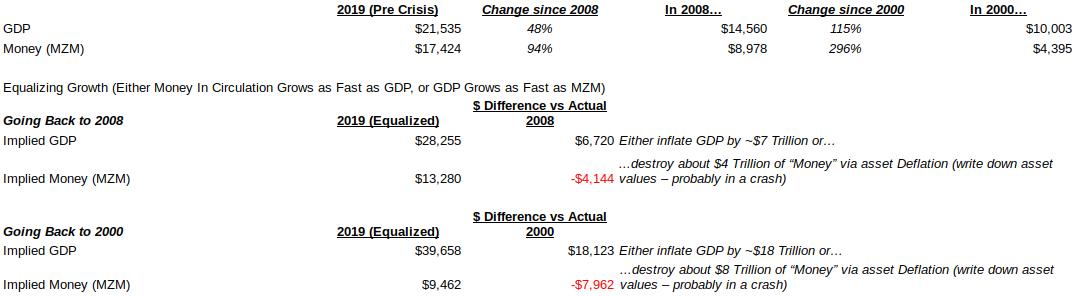

There is a lot more cash-per-dollar-of-GDP sitting around than there used to be. Since 2008, the amount of money sitting around has doubled (+100%). The real economy has only grown by half (+50%). All as measured by declining monetary velocity (see prior post for the velocity data etc. here).

Since 2008, GDP has grown 48%. Money has grown by 94%.

Since 2000, GDP has grown 115%. Money has grown by 296%.

Most of the “excess” money has been created via the various Fed interventions especially Quantitative Easing (QE). Fed Chair Ben Bernanke once said; “The problem with QE is it works in practice, but it doesn’t work in theory.” In other words, the placebo effect.

All these numbers are up to 2019. Pre-COVID.

“Money” here means ready cash. MZM – US bank deposits, checking accounts, money market funds, etc… Notably, it does not include money sitting at the Fed (“excess reserves”).

The scale of that mismatch suggests a Bezzle does exist. The above gives us a guesstimate measure of the (inherently un-measurable) Bezzle. A lot of paper wealth sitting around that isn’t backed up by the real economy. An increasingly fat jockey on an increasingly enfeebled horse.

If GDP and money had stayed in rough balance, either GDP today would be much higher or Money would be much smaller. The difference might give us a rough estimate of the Bezzle. If we make the (potentially very false) assumption those two number series re-synchronize, then the catch-up-effect requires that…

…either nominal GDP grows much faster to catch up with the money supply (inflating away the value of those “Bezzle” assets)

…or a big chunk of paper wealth evaporates to shrink “money” back down to proportion with GDP (deflating those “Bezzle” asset values by potentially violent write-downs).

In dollar terms, we either need to write off $4 to $8 trillion of “Bezzle” paper wealth, or inflate the Bezzle away by increasing nominal GDP by $7 to $18 trillion (with no real dollar increase in wealth). This assumes a catch-up effect. Either we grow nominal GDP faster than “money” or we shrink “money” to re-proportion it to GDP. For context, GDP in 2019 was $21.4 Trillion. So destroying $4 to $8 trillion of paper wealth is 20%-40% of one year’s GDP. Brutal and worryingly plausible in size.

The longer we keep this up, the bigger those stagnant pools of paper wealth get. Making for an uglier reckoning. This is the problem with any embezzlement or Ponzi scheme. The numbers eventually compound until the edifice collapses under its own weight. Which is arguably why the policy response to COVID has been so frantic. Trying to push an ugly reckoning into the future. Piling up more Bezzle that will, eventually, have to be destroyed via the fires of asset write-downs or the freezer rot of inflation. Or, maybe, more wisely, trying to over-print enough to tilt a resolution in the direction of (less-destructive) inflation instead of deflation.

Either way, we are left with that fat jockey on that thin horse. The jockey is getting fatter and fatter. Eventually the horse must falter. Maybe not this crisis. But sometime somewhere.

This crisis might be big enough to force the issue. We’ve seen a huge move into stocks recently. At a time the real economy looks extremely shaky. We all know the stock market can be an incredibly efficient money destruction machine. One day you wake up and 30% of it just is gone. Poof. Like what happened in, say, March 2020.

It might not happen through stocks. Real Estate and Bank Loan markets take longer to adjust (it took ages in 2008-2011). But all asset markets will, eventually, do their job of destroying paper wealth that isn’t supported by real-world cash flows. Usually over-correcting downwards before leveling out. So we could “lose” $8 to $16 trillion (on a $21.5 Trillion GDP), and bounce back up from there.

There is a huge mental chasm between a “temporary market pullback” and a “permanent loss of wealth.” People will spend through a pullback. But if/as they figure out the Bezzle is never coming back… Same quote below with a different sentence in bold. It could foretell a much less exuberant future…

“At any given time there exists an inventory of undiscovered embezzlement [not the illegal kind. The legal, clever Wall Street kind. Think 2008’s mortgage backed bond bubble] in — or more precisely not in — the country’s businesses and banks. This inventory — it should perhaps be called the bezzle — amounts at any moment to many millions of dollars. It also varies in size with the business cycle. In good times people are relaxed, trusting, and money is plentiful. But even though money is plentiful, there are always many people who need more. Under these circumstances the rate of embezzlement grows, the rate of discovery falls off, and the bezzle increases rapidly. In depression all this is reversed. Money is watched with a narrow, suspicious eye. The man who handles it is assumed to be dishonest until he proves himself otherwise. Audits are penetrating and meticulous. Commercial morality is enormously improved. The bezzle shrinks.https://www.goodreads.com/quotes/tag/bezzle

We might avoid a resolution this time around. We did in 2008. Extend and pretend… Moreover, this piece could just be howlingly wrong. Please push back. And/or please forward this on to someone/anyone who might be able to push back at it (please forward me the replies no mater how brutal). I’ll learn the most from the push back. Two immediate caveats where I am obviously “wrong.”

There are all sorts of valid reasons why money supply and monetary velocity might never rebound. Big permanent demographic shifts especially. Also the impact of low rates, foreign trade, etc… So the ENTIRE underlying premise here is also questionable. Still interesting perhaps. But there is no God-given reason this catch-up effect must happen.

This is in no ways a “valid” economic analysis. A real economist would justifiably tear this whole piece to shreds. But the worship of false precision is the hobgoblin of small minds (and most Economics departments). I still think this sort of “analytically leaky but directionally interesting” analysis has value. It is clearly faulty, but it shines a light on something we otherwise can’t measure. So it might remain useful.

Posted inUncategorized|Comments Off on The Bezzle. Either Inflate By $7-$18 Trillion or Bonfire Away $4-$8 Trillion of Paper Wealth. Is This What Velocity is Telling Us?

Good fortune is good in-laws 🙂 I’ve had a little more time to read in the last few months (courtesy of the aforementioned in-laws). I figured I’d share. Forgive any typos below – this small laptop keyboard and my machine gun typing style don’t go so well together.

Strongest recommendation would be “Biggest Bluff” and then the combo of “Alchemy” and “Trade Wars.” The MMT book is less consistently strong, but worth it for its first few head-exploding chapters.

BIggest Bluff: Psychology PHD turned New Yorker staff writer with no poker experience decides to try and play in the world series of poker in one year. The book itself is much less about poker than about life, risk, etc. Great meditation on a lot of elements that also touch on investing. Found its really helped me feel OK with sitting out the last few months in particular so timely. Very readable.

I’m going to present the next three books in the order that I read them because they ended up layering nicely on each other.

The End of Alchemy: Books saying the world has become imbalanced and we are all headed for a big reckoning are a dime a dozen. Usually written by some tinfoil hat crank. They are almost never well researched, reasonable, carefully argued thoughts from the retired head of the Bank of England (Meryvn King). THis book gave me “permission” really start worrying about stuff. t is skimmable in places, but very readable and an excellent macro 101 piece too if your last money and banking class was back in college.

Trade Wars are Class Wars: Ignore the title, it is not a political polemic. It is an extremely readable look at how international trade imbalances and domestic income imbalances are driving the world economy in a can’t-go-on-forever unsustainable direction. Most refreshing is that the US ends up almost a passive victim in this telling – “forced” to over-consume and over-borrow by the surplu-producing Chinese and Germans and wealthy elites). THis follows on from King’s book and points you to where the imbalances are building. THey pull their punches a bit about how it all unwinds (one author teaches in China and I guess wanted to keep his job), but it clearly doesn’t unwind well for anyone.

The Deficit Myth: Written by the main proponent of MMT economics. Guaranteed to change how you think about money, deficits, the economy, stimulus, the role of government, etc. You may not necessarily agree with her and there is way too much not-as-well-supported policy commentary mixed in. But there are some real Plato’s cave moments in here too. And explains the (valid) core argument of MMT, which is that the ONLY things that matters is the real economy’s productive capacity. “Money” per se doesn’t really matter. Milton Friedman said “Inflation is always a monetary phenomenon.” MMT turns that on its head to say “Inflation is always a real economy productive capacity phenomenon.” Outside of true Weimar Germany Zimbabwe style money printing hyper inflations, that MMT formulation seems like a much more useful construct for looking at the world. You probably won’t agree with some of her policy suggestions. But you really will never look at the (economic) world the same way again. Extremely readable too.

I have this book teed up for when I get home. Meryvn King (BofE) and John Kay (FT). Argues against the increasing tendency to equate “risk” with “volatility” in financial markets. After that I’m not sure where it goes but Mervyn King is a smart guy so….

Posted inUncategorized|Comments Off on Book Recommendations

{kind=link}