I am setting out on a drive across the USA to Virginia to visit the in-laws. Maintaining our quarantine bubble in a 19 foot Sprinter RV that a friend was generous (and crazy) enough to lend us. With a 5 month old and 2 1/2 year old strapped into car seats for the ride. It will be “interesting” for sure. And hopefully even fun. So I’ll be off the grid for a while here.

I’ve got two posts teed up. I’ll just push them out today.

Posted inUncategorized|Comments Off on Heading Out Across America

We’ve all seen the “USA is in Global Decline Versus China” pieces. Now mostly with a COVID spin on them. I wrote this up as a strawman counter-argument. I’m not entirely sure I believe this argument, but figured I’d share it.

COVID could end up actually IMPROVING the world order. Leave the US Less Powerful, But Still Hegemon of a More Robust World Order.

Here’s the logic (vs the “decline” argument).

Point of agreement. Trump and the virus response has unquestionably destroyed global complacency about the US’s ability to act as a global backstop. The 737 Max destroyed confidence in the FAA. CoVID destroyed confidence in the CDC. Etc Etc. Lets hope the economic crisis doesn’t destroys confidence in the Fed (weak grin). BTW, I blame Trump less than 40 years of “starve the beast” assaults on government apparatus, but that is water under the bridge.

However. COVID has ALSO destroyed any faith we could have in China. Their credibility has been even MORE shattered – especially from a “auditioning for a role as the new hegemon” perspective. COVID (and other actions) show China’s institutions are totally unqualified to replace the FAA, CDC, Fed, etc…

So that leaves the US as the only game in town. But a substantially less comforting one. To quote Reagan, other countries will have to “trust but verify” instead of just blindly accepting whatever the US says (That new 737 is just fine to fly! Take our word for it!).

A new era of mutually self-reinforcing realism? That leaves the rest of the world working a little harder towards the collective global self interest. The US remains “first among equals” but everyone else raises their game instead of free-riding on the US’s policy direction. Countries invest in their own aviation authorities, CDC’s, defence capabilities, and the like.

That makes life more complicated for the US, but it also spreads the burden and introduces much-needed heterogeneity and resilience into the system

Oddly, in that scenario China probably ends up even more frozen out. If everyone else raises their game to be less dependent on the US, they also need depend less of China.

I’m reminded a bit of how Microsoft reigned supreme as “the” trusted hegemon in compute for so long. Then we all collectively figured out a lot of their stuff was absolute crap. Up came Apple OS and Linux and all sorts of other heterogeneity. Computing is a LOT better off for that diversity. Making us ALL better off. Arguably even MSFT is better off shouldering less of that burden.

Although the slogan “Make America Less Great, Making the Rest of the World Greater, Making For a More Robust System.” doesn’t quite roll off the tongue. Nor does it fit on a hat.

Posted inUncategorized|Comments Off on COVID and US Decline Vs China and Etc….

Stripped of euphemism, America has pretty clearly made a choice. To “save thewealth (ahem) “the economy!” at the expense of “a few million dead.” Chasing the possible chimera of herd immunity.

The problem is that is a false choice. We will definitely get the millions of dead. But we probably don’t save the wealth. The worst of both worlds.

A month or so ago, I really did not think “we” (or our elites) would make this choice. A failure of imagination on my part. Regardless, I’ll stay hunkered down and hopefully we’ll avoid the worst of the consequences. And I’ll continue to hope that I am wrong (about the death stuff especially, less so the wealth stuff).

We Have Chosen the “Herd Immunity” Strategy. Lots of Dead People Fast.

Forced to make a choice, America has chosen to preserve the wealth “the economy.” Sacrificing a lot few million ordinary lives on the altar of mammon. Lets not pretend otherwise. Governor Kemp of Georgia and others knew what they were choosing with “early re-opening.”

2-3 Million Dead: The USA (or large parts of it) have pretty clearly chosen to let the pandemic run its course. Meaning we are choosing 2 to 3 million extra deaths (assume a ~1% fatality rate and 80% infection rate before we get some sort of herd immunity).

Why sacrifice those lives? We (OK our leaders and the elites they listen too) are making wealth preservation a priority. What sort of wealth? Small-fish-nationally, big-fish-locally, “country club Republican” wealth. The strip-mall owners looking into the abyss of personal bankruptcy if those store rents aren’t get paid. The car dealers paying the carrying costs of unsold cars. The McDonalds franchise owners who face a HUGE balloon payment of rent in midsummer. The sort of person who can call the Governor and be put through.

Assuming it won’t be “our” sacrifice. Underlying that is the personal calculus that the bulk of those deaths will happen to poorer people living in more crowded spaces. These decisions are sending “them” out to do that dying, not “us.” No shared sacrifice here.

I’m no epidemiologist, but a lot of those deaths will probably happen in the next 6-12 months. Before a vaccine is readily available in 2021.

The whole idea of herd immunity might prove to be a mirage. It isn’t clear prior infection provides protection. It might. It might not. We simply don’t know.

Having made that choice, we are now indulging in a (probably brief) period of magical thinking. Somehow we’ll save our asset values and the virus will fade away in the summer heat! This optimism seems to be what is powering the current market boom. The consequences of that choice will likely hit hard in the weeks and months to come.

Will it Work? NO? The Economy Will Still Tank. Those Strip Mall Landlords and McDonalds Franchisees Are Still Going Bust.

Forget the morality. Just ask whether this gamble will pay off. If we “re-open” the economy, will it actually re-start? No. It probably won’t. We’ll wheeze and struggle and stop-start along. The worst of both worlds.

The magical thinking here is “they” will gladly, boldly, bravely march out to face death (heading back to Disneyland), while “we” cower behind closed doors (aided by Instacart, Amazon, and remote working).

All evidence suggests “they” aren’t going to go out (and get infected and die) with enough enthusiasm to really re-start the economy. “They” will stay home. We will limp along. The rents won’t get paid. The wealth will still evaporate. Same outcome as a lockdown, but with more dead people. And more angry, bereaved survivors (and voters) left behind.

Look at the Google Mobility data from Sweden, which keeps being cited as a model by the “no shutdown” crowd. Ignore the anecdotes and look at the facts. Swedish people are social distancing anyway because they aren’t f**ing stupid! Retail traffic is “only” down 13%, traffic in parks is UP 82%, transit stations down 31%. Workplaces down 11%. That all translates into a pretty sluggish economy IMHO.

(Breaking News Today) Look At the Google Mobility Data for the state of Georgia. They lifted their lockdown a week ago. Folks in Georgia are not flocking out into the streets. Retail shopping traffic improved, but its still seriously depressed at down 23% statewide. Ominously workplace traffic actually FELL from -36% to -45% statewide. Atlanta data is much worse in general and workplace is now -60% vs -45%?!? The data are particularly ominous given assumed “pent up demand” for things like haircuts.

Fulton county (Atlanta) has Retail and Recreation down 43% (was -52%), Transit down 55% (no change), parks down 45% (was -41%), workplace down 60% (was -44%?!?).

State-wide has Retail and Recreation down 23% (was 34%), Transit down 44% (was 53%), parks down 15% (was +4%), workplace down 45% (was 36%).

Those folks will go out and mingle. And infect each other. Meaning disproportionate pain for places where disbelief is highest. Driving a summer of highly local, “mini New York” crises shutting down cities and towns and counties. Particularly in Red States.

All of the above (especially the Georgia data) doesn’t solve for a re-started economy. Or a V-Shaped recovery. It solves for the economic equivalent of the “limp home mode” of your car (a real thing – computer limited to ~30 MPH for a limited period of operating time). It sucks.

“Everybody has a plan until they get punched in the face.” (Mike Tyson)

We’ve made our choice. Sure a lot of people will die. But it will mostly be “them” not “us.” And maybe some miracle will save my wealth “the economy.”

So we’ve got our plan. The only question is how long it takes for us to get punched in the face…

Sigh…

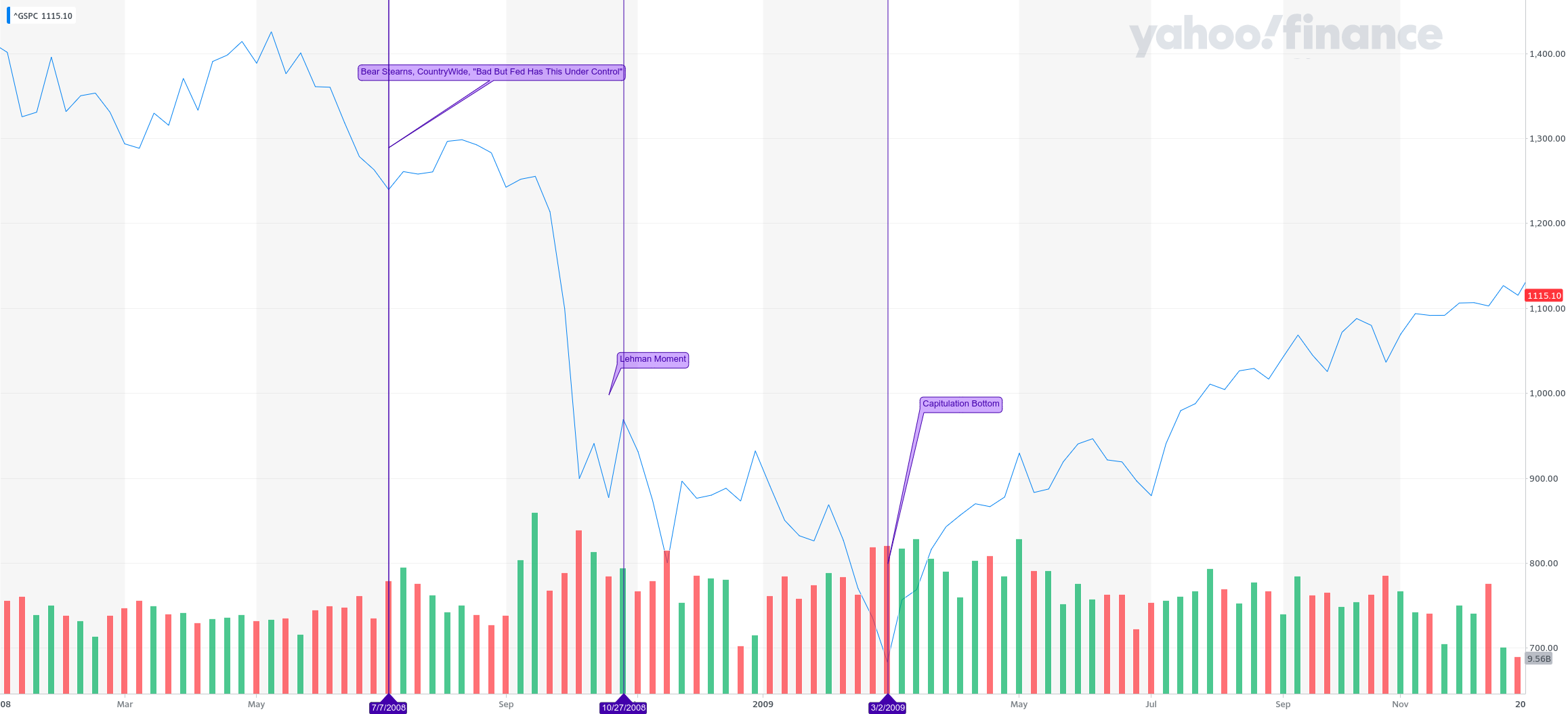

The Market – We’re Having Our Bear Stearns Moment Now. The Lehman Moment Comes Later (If it Comes).

The stocks I sold a few weeks ago are now HIGHER than they were in January. That is… (ahem)… frustrating.

But I keep reminding myself that the market chugged merrily along after Bear Stearns and Countrywide went bust in March 2008. We thought we’d avoided a systemic crisis. Doing the Wile Coyote (link below). Lehman’s bankruptcy, in September 2008, is when Wile stopped levitating. He hit bottom in March 2009. See my post here.

Maybe I’m wrong. Maybe we don’t have a systemic crisis. The Lehman moment may never come. But I’m going to stay on solid ground for a while now just in case. Meep Meep.

<a href=”/gif/wile-e-coyote-falls-off-cliff-GJZK50″ title=”Wile E. Coyote falls off cliff”><img src=”https://i.makeagif.com/media/5-15-2015/GJZK50.gif” alt=”Wile E. Coyote falls off cliff”></a><div style=”font-size:11px;”>make <a href=”/” title=”make a gif”>funny GIFs</a> like this at MakeaGif</div>

Posted inUncategorized|Comments Off on The Worst of Both Worlds? America Likely Choosing ~2 Million Dead AND Huge Economic Losses.

There are three basic inputs to any economy. Land, Labor, and Capital. This crisis is a massive economic shock. So who takes the hit? Land? Labor? Capital? That is the un-stated question driving the whole “re-start the economy” debate.

81% of Americans (the Labor) think Capital (and Land) should take the hit.

Per this Politico poll.

“eight in 10 voters, 81 percent, say Americans “should continue to social distance for as long as is needed to curb the spread of coronavirus, even if it means continued damage to the economy.” Only 10 percent say Americans “should stop social distancing to stimulate the economy, even if it means increasing the spread of coronavirus.” Nine percent of voters have no opinion.” https://www.politico.com/news/2020/04/15/poll-dont-stop-social-distancing-coronavirus-spread-187290

Lets say a quick “wow” about the 9% who have “no opinion.” Then move on to guess at what 10% who put the economy first. They probably map pretty tightly to the top 10% in…

…Income, especially passive income (real estate rental and dividend checks)

…Asset ownership – especially commercial and rental real estate.

…Personal freedom to work from home and thus self-isolate until 2021.

Reading on, lets all remember the top 10% (the elites) isn’t particularly beloved by the bottom 80% (the deplorables).

Why is the the other 80% putting health and safety over “the economy?” These folks all work paycheck to paycheck anyway. Their non-existent stocks of wealth/capital aren’t going to take a hit. They are also probably starting to figure out that…

…the unemployment checks will keep coming

…they can hang on OK on that for 6-12 months – especially if they don’t pay their rent/mortgage/credit-card bills.

A Collectively Declared Debt Holiday is the Real Motivating Fear.

The non-payment bit is what really gives the top 10% the heebie jeebies. 31% of America’s renters didn’t pay their rent in April. It’ll be 40%-50% in May. By June, even people who can afford to pay will be asking themselves “why am I being a chump? No-one else here at Slumlord Towers is doing it!”

If enough people stop paying, there is no way that top 10% can ever go back and collect. Nor will it negatively impact credit reports because “everyone” is going to have the same non-payment history at the same time. Same goes for credit card bills and most other debts.

That growing wave of non-payment helps us work back to answer this question;

What dark fate is so threatening that 10% of Americans polled would see a higher death rate as preferable?

Capitalism Red in Tooth And Claw Working its Magic On “Us,” Not “Them.”

The threat is clear and, to my mind. highly likely. A major, permanent write-down in the value of wealth-creating assets (especially commercial real estate). Martin Luther King frames the issue better than I can.

“We all too often have socialism for the rich and rugged free market capitalism for the poor.” ― Martin Luther King Jr.

Except, this time around, capitalism is likely to eat its own. The poor will have it tough. But they will eventually go back to living paycheck to paycheck. The rich, however, will suffer a permanent loss of wealth.

A Long Partial Shut Down (Official Or Informal) => A Massive Un-Rented Real Estate Glut => Massive Rent Reductions on Re-Start => Massive Wealth Destruction.

Think about commercial real estate in particular. There is about $6 Trillion of it in the United States. It underpins a LOT of wealth. But no spin-meister on earth is good enough to make Landlords into a sympathetic class deserving of a bailout.

The immediate crisis is the mortgage note is still due, but the rental income isn’t coming in. In a few months, that lands most landlords in bankruptcy.

If you survive that, commercial landlords will find themselves with largely empty strip malls, malls, hotels, and other buildings that are incredibly hard to re-purpose. In other words, a MASSIVE SUPPLY GLUT. That will take years to work down. When the economy re-starts, prospective businesses owners will have their pick of locations and all the negotiating leverage on rent. Even if all the old tenants just come back, they’ll do it having negotiated lower rents by threatening to NOT come back. That is a permanent write-down of wealth.

Residential landlords will probably do better out of it. There will still be a supply glut (all those service industry types who moved back home etc…). So they won’t be able to collect back rent. Better to keep the tenants you have and just try to get them back to paying. But that supply glut also creates downward pressure on rents. People will shop around, upgrade, etc…

Don’t Kid Yourself, We Will Have A Long Partial Shut Down (And So a Write-Down).

Even if people “go back to work,” they don’t have to go out to dinner. Or go to Disney. or go to a movie. Or fly. Or go to a hotel.

Until we have a vaccine, they won’t. Or they won’t do it as much.

That means a lot of service industry businesses (which occupy much of that commercial real estate) will stay shut down. Which means a lot of service workers (disproportionately renters) won’t get re-hired. In other words, we’ll stay partially shut down.

Those closed service business won’t be sending in their rent checks. Those service industry non-workers won’t either.

Medical Advances Make a Partial Shut-Down MORE Likely Until a Vaccine in 2021.

The usual retort here is some hopeful medical claim. “But I hear trials of XXX are going well! J&J says a vaccine will be approved by 1Q 2021…” That is all good news, although you and I probably don’t get anywhere NEAR a vaccine shot until mid-2021.

But stop and think for a second. If we are really going to be OK in 6-12 months, then why go out and risk your life in the meantime? If the virus is a long-term fact of life, you might take the risk. But if it isn’t a risk by 2021, you’re an idiot to NOT hunker down and wait for the vaccine.

So the “positive medical developments” arguments just reinforce the likelihood of a (self-declared) partial shut-down.

Capitalism Probably Comes for the Capitalists This Time Around.

In the last crisis, the bailout got bent in favor of the top 10%. There are a lot of really smart people working overtime to figure out how to do that again this time.

SO far, all they’ve come up with so far is the thin gruel of “consider the emotional toll of all those people out of work! The suicides! The alcoholism!” That transparently self-serving concern isn’t going to change a lot of minds.

The poll above suggests that messaging battle has already been lost. That 81% seem to understand that “getting the economy re-started” means “me and mine might end up dying for no good reason. We’re a rich country. We can just keep writing them trillion dollar checks. They’ve been doing it for years to line their own pockets. And I ain’t never seen it coming to me. So its our turn now…”

The problem is that logic is entirely correct. We can keep writing those unemployment checks. We will.

That means someone will take a massive loss. But absent a massive bailout, that loss will mostly hit the landlords, bosses, and the bosses’ bosses. In a normal year, Congress could be counted on to figure out some sort of bailout. Congresscritters own a lot of that commercial Real Estate themselves. The President does too.

But it isn’t a normal year, its an election year.

All the 81% has to “do” is make sure the politicians keep sending the bailout unemployment money to them (Labor) and not the top 10% (Land and Capital). With an election coming in November, they have the means to enforce that. And punish any bailout of Capital big enough to make a difference. Especially as a bailout of landlords and REITS and Debt Investors will be much harder to hide behind smoke and mirrors vs 2008’s bailout of the banks.

Posted inUncategorized|Comments Off on Is Capitalism Is Coming for the Capitalists? 81% of Americans Seem To Think So.

I keep running into variations on the “quick in and out” economic scenario. Most disturbingly among professional investors and other people who should know better. Per prior posts, I think this reflects a consensus that hasn’t moved past the “Denial” phase of the stages of grief (followed by Anger, Bargaining, Depression, and Acceptance).

I see a long, sluggish recession as the most likely scenario after so much economic disruption.

Consensus seems to expect a quick in-and-out. I think that is insane. The economic equivalent of WW1’s “The war will be over by Christmas… 1914 1915 1916 1917 1918.” Here’s a reality check you can try at home.

When Do You Think Disneyworld Will Re-Open?

Keep in mind the park only works with a certain (very large, continuous) volume of people flowing through it. My answer is either:

After we have a widely available vaccine – so 2021 at earliest given production ramp-up times etc…

Shortly before we go through another massive resurgence of the virus (sparking and another economic tailspin). Maybe after a “Economic Grand Re-Opening” in late summer keyed to a desperate effort to re-elect Trump.

Neither scenario above solves for getting back to normalcy in the next 6-12 months. Which also doesn’t solve for a return to prior valuation levels – the Fed’s dollars be damned.

Of course, the investment professionals might be (cynically) forecasting the false dawn of that Trump re-election gambit in mid-summer. I’m less convinced. Why? I don’t think the little people are quite that stupid or desperate.

The “Stupid People” and Little People” Hypotheses

Implicit in the v-shaped recovery are also two morally suspect but, more importantly, factually suspect hypotheses.

The “stupid people hypothesis.”

I’m smart enough to stay home until we have a vaccine, but “those people” are so dumb they will go out the first chance they get. And stay out when reinfections start up again…

The “sacrifice the little people” hypothesis.

I can work from home. The little people in services jobs can’t, but they don’t have savings. Poverty will force them to go out and start working again. Sure we’ll lose a few million of “them” to the disease, but [emerging elite dogma phrase here] we can’t make the cure worse than the disease. Especially as I’m making the comfortable assumption me and mine won’t be doing the dying in service of preserving my wealth (ahem) the economy…

Both rest on assumptions that don’t stand up to common sense.

They aren’t that stupid. They love their elders/children too. Yes, people will go out “more” after a total lock-down. But they are going to stay pulled-back until we get a vaccine. Which translates into sluggish economic activity. And no Disney World.

If “you” don’t go out, “they” won’t have jobs to go back to. Top 10%’s spending is what creates many of those little people jobs. Waiters without customers don’t stay employed for long. The guy who plays Mickie Mouse won’t get re-hired until Disney re-opens. Our (massive) service economy is heavily weighted towards many less-affluent people (the presumed stupid and desperate) providing services to a much smaller slice of affluent people (the presumed smart, work-at-home, still employed, socially distancing people). If “they” go back out and “you” stay home, the equation doesn’t balance.

So far, however, comfortable v-shaped assumptions seem to be winning out over logic. Because Denial.

I’m guessing the rosy scenario will die a death of a thousand cuts sometime by late April. We start quarterly corporate earnings season next week. That will replace assumptions with facts. Massive economic damage already done in March and a total lack of visibility into the months ahead.

What Will the “Anger” Stage of Grief Look Like For the Affluent Class? Not Sure.

It is pretty easy to envision the “Anger” stage of grief for the masses. They will get (even more) angry at the elites. See this piece here for a model and a well-argued case for how the Left should harness it. https://theintercept.com/2020/04/05/coronavirus-american-politics-democratic-party-biden-sanders/

But I struggle to see what “Anger” will look like for the comfortable classes. Because they are (or were) pretty comfortable. Not much given to anger. And they can’t well get angry at the elites because they ARE the elites. I’m guessing there will be some sort of scapegoating (probably of Trump). But I’m not sure that is going to really suffice.

We live in interesting times.

Posted inUncategorized|Comments Off on When Do You Think Disney World Re-Opens? An Economic Reality Check.

I did a “starve the beast” post from a few weeks ago. “We starved the beast. And suddenly we find we need it. But no amount of whipping is going to get it moving any faster than the starved, weak, abused thing we let it become.

This Washington Post piece nicely sums up that starved, weak, abused response to date.

“Small-business owners have reported delays in getting approved for loans without which they will close their doors, while others say they have been denied altogether by their lenders and do not understand why. The law’s provision to boost unemployment benefits has become tangled in dated and overwhelmed state bureaucracies, as an unprecedented avalanche of jobless Americans seeks aid,” Jeff Stein reports. “Officials at the Internal Revenue Service have warned that $1,200 relief checks may not reach many Americans until August or September if they haven’t already given their direct-deposit information to the government. Taxpayers in need of answers from the IRS amid a rapidly changing job market are encountering dysfunctional government websites and unresponsive call centers that have become understaffed as federal workers stay home. … More than a dozen senior positions in Treasury were unfilled heading into the crisis, creating a wide vacuum between the career staff and the highest levels of management. …

Were do we go from here? The Facts Won’t Win Anything. The More Effective Messaging Will Win.

There is only a rational, constructive, “right” path. And there is a self-serving, ultimately self-destructive, “wrong” path.

Effective, competent government matters. We need to invest!

I told you the government can’t do anything! We need to keep tearing it down!

We’ve been on the wrong path for about 30 years. Because it serves the interests of a narrow but powerful slice of people. Folks who tend to own the loudest megaphones. That negative message is still unquestioned dogma among too many otherwise sensible people. That scares me a lot.

Joe Biden also doesn’t strike me as the kind of guy who’s going to lead the charge for “real” change (vs tinkering around the edges). That scares me a lot too.

We all need to put our shoulders in to push back. Thousands of people have died because we starved the beast. If that isn’t enough to motivate folks, I’m not sure what will.

Posted inUncategorized|Comments Off on “Starve the Beast!” Comes Home to Roost. But Who Will They Blame?

To date, I’ve seen far too much amateur epidemiology and surprisingly little economic analysis around Coronavirus. Even the econ blogs I follow have fallen victim to this disease (armchair virology, not Coronavirus). In doing so, they have also fallen strangely silent on the economic outlook.

I’ve experienced the same dynamic in conversation – even with professional investors. If you bring up the economic and financial outlook, conversation limps along for a few sentences of vague foreboding. Then it slides back to discussing the latest hopes for a miracle cure!!!! After repeated tries (I’m not the most clueful guy), I’ve figured out that people just don’t want to go there (yet).

Why? Stages of Grief. Denial, Anger, Bargaining, Depression, and Acceptance.

We are going through two distinct grief cycles. One track on the virus. One track on the economy. We are at different stages of grief on each…

Virus => Denial, anger, Bargaining (new drugs!, vaccine coming!LL Bean is making masks!), depression, acceptance.

Economic recession to come => Denial (NO NO NO Lets get back to talking about the virus!!!), anger, bargaining, depression, acceptance.

We are also doing what humans do – hyper focusing on an (admittedly serious) immediate threat to the exclusion of an (arguably natier) secondary threat.

At some point, however, the economic news is going to get hard to ignore. Because something like 20-30 million newly unemployed folks (out of ~156m total employed) are going to be walking among us by the end of April. Having mostly lost health insurance (stupidly and inexcusably tied to employment ONLY in the US). During a nationwide pandemic.

As a society, we’ll move on to the next stage – Anger. That is not gonna be fun.

A possible silver lining is that anger will probably be directed at the fools who led us into this so ill-prepared. But we’d be foolish to expect that anger to be wholly reasonable in choosing its focus and target(s). Especially with the fool(s) at the top desperately working to channel that anger away towards someone, anyone else. We can only hope they fail in that effort too.

We live in interesting times.

Posted inUncategorized|Comments Off on Stages of Grief. We’ve Hit “Bargaining” On the Virus. Only at “Denial” On the Economic Impact.

Someone with more emotional intelligence than I noted that my last blog post could have read as saying;

“I’m selling out now because I know I’ll be able to call the bottom again (because I am oh-so-smart).”

That was absolutely NOT my intended message. The intended message was.

I’m not so foolish as to bet I’ll call “the bottom” again. We might not even get to a true capitulation bottom. But I do know what a capitulation bottom feels like. We aren’t anywhere close now. There is far too much hope out there. People buying the dip. Talk of a quick return to work. Wonder cures just on the horizon…

I have no idea if I’m doing the right thing (by going to cash). But I do think I’m making the right decision based on; 1). no visibility. 2). a binary future scenario with a pretty awful downside case (see below).

If the economy rides through OK, I’ll be wrong. I’ll miss a rally.

If the economy (more likely) take an ugly hit, we have one or more legs down from here.

When/if things really feel hopeless, I’ll force myself to buy back in. No idea if I catch “the bottom.” It could just keep getting worse from there. But we’ll definitely be closer to a bottom than we are now…

Capitulation bottoms are marked by numb despair, resignation and indifference. The result of a long siege of fear. All assets are being liquidated, with correlations at 1. We all lived that in early 2009. We may not get there, but we definitely aren’t there now.

We May Not See the Capitulation Part

The market is swinging wildly because it is pricing in binary scenarios.

Optimistic: The economy bounces back quickly. Limited damage done. That scenario is driving market rallies. “Buy the dip!”

Bad-to-Catastrophic: The shut-down drags on until we have a viable vaccine in wide distribution (in other words, 2021). That likely leads to a downturn that dwarfs 2008. The “catastrophic” flavor of the downside scenario hasn’t been priced in yet at all (IMHO).

We aren’t sure which scenario plays out. The market will almost certainly figure it out (and price it in) before I figure it out. What we DO know is the potential cost of the negative scenario vastly outweighs the potential benefit of the positive scenario.

Given that cost/benefit, the “smart” decision is to plan for that negative meltdown scenario. It might not turn out to be the “right” decision after the fact. But I’d prefer to miss a rally than suffer a melt-down.

OK, I Do Think We Will See Capitulation – This Likely Gets Bad.

My metaphor for the coronavirus crisis is the 1906 San Francisco earthquake. The earthquake was bad, but most of the damage was done by the fires that followed it. The virus is the earthquake. The resulting economic dislocation are the fires. Absent a miracle cure, I don’t think the likely scope of the upcoming economic crisis is understood much less priced in.

My worry is its economic shock and the resulting stresses on the financial system. If a plane hits too much turbulence for too long, something big – wings, an engine – eventually falls off. We know a lot more about that than most folks want to admit (yet).

The longer the virus crisis drags on, the worse the economic crisis gets. The fires after the earthquake.

The worse the real-world economic crisis gets, the more likely we spark a financial crisis. Gasoline on the fire. That is why I am using 2008 as a template.

The usual counter-argument here centers on some sort of medical miracle breakthrough. But we also know it’ll take until 2021 for a vaccine to be developed, pass trials, and get widespread distribution to the population at large.

I also think we all know (but aren’t yet willing to admit) that economic activity will remain depressed until there is a vaccine. A “therapeutic” treatment is great news, but “you still might end up on a ventilator and die, but it is less likely” doesn’t read like a banner under which people march back out unafraid.

Worse than 2008? Hard to See Why It Wouldn’t Be…

The other thing we know is the global Coronavirus crisis is clearly a broader-based and sharper economic shock than the US’s 2008 mortgage crisis. This doesn’t guarantee a “worse” economic result. But it does mean the real possibility of an equally or more catastrophic scenario. That is the downside case I have decided to protect myself from.

I worry we are in the March 2008 “Bear Stearns goes bankrupt – what a pity” phase where everything still seemed under control (economically). If the economic stress overwhelms the system, we could have a October 2008 “Lehman Moment” out there somewhere. Followed by the long ugly siege of selling that took us to that March 2009 bottom.

I Don’t Know Any Better Than You, But We Need to Decide Now – Not Knowing.

In short, I’ve decided to “risk missing a rally” to avoid risking a disaster scenario.

That isn’t to say that companies (like NET) aren’t going to have a great quarter and a pretty good year. They probably will. But they report 6 weeks from now. That’s an eternity in Coronavirus time.

Looking out over a year, those good numbers will matter even less if we get a repeat of 2009 – correlations go to 1 in liquidation selling. Everything gets sold and everything goes down. A capitulation bottom starts with capitulation. That is an ugly, multi-month process.

We are facing a binary outcome here. One of those binary scenarios is a possible systemic financial crisis so dire that, in response to the threat, the Fed has opened up every tap it has, the Republican Senate just passed a $2 trillion stimulus bill without a blink, and even Trump is taking it seriously. That scenario has clearly gotten folks very very scared.

I’m not saying that super-bad scenario WILL happen. I have no idea. But better to plan for what happens if it does. If it doesn’t, you miss a rally. If it DOES, the bottom is a long way down and no asset will hold up well. We’ll see. At least I’ll sleep better.

(Recap) How I Called the Bottom in 2009. It Just Couldn’t Get Any Worse.

Lets be clear about the ONLY thing I knew writing that “calling the bottom” note back in March 2009. I had NO IDEA when it would get better. I just knew it couldn’t get (much) worse. The title says it all.

“My Centre is Yielding. My Right is Retreating. Situation Excellent. I Attack!”

Sometimes attacking is the only defense you have left.

We’d already been though months of liquidation in markets. All sellers, no buyers. That week in March, two of the networking equipment companies I covered told me customers were making capital plans on a rolling two week basis (vs a typical 1-3 years). In other words, the demand and planning horizon had shortened about as far as practically possible. It couldn’t get shorter. It couldn’t get worse. Abject fear.

That is what a bottom looked like back then. It might end up being what one looks like now. And we aren’t close to that yet. I hope I’m wrong.

Posted inUncategorized|Comments Off on I Have No Idea If I’ll Call The Bottom This Time. I Do Know We Aren’t At a Capitulation Bottom Now.

I am tired/frustrated/surprised when I hear people say “Well, we don’t really know what will happen [about the next 6-12 months].” That simply isn’t true.

A lot of people are going to die. The economy is going to take a brutal hit. An economic hit big enough to spark some sort of systemic financial crisis.

OK, we don’t know the specifics. But we know the above. Does more specificity really matter? Following from that, a grab bag of mostly political and thoughts below.

We May Get a Medical Miracle? But That Won’t Deliver Us an Economic Miracle.

The wild card is some sort of effective treatment like Remdesivir. But even if that bends the curve, it will take a while to ramp production, the healthcare system will still buckle, nd some land mine in Finance still probably goes off. The economic damage will still be huge. A medical miracle would save a lot of lives, but it probably won’t save the incumbents.

Politically, We Already Know a Lot Also.

The election in November will pivot on Healthcare (for sure) and “bailouts” (at least the Democrats messaging). A referendum on February 2020 – November 4th. Like 2008, a bonfire of the incumbents – particularly for the party in charge [Republicans].

Why do we know this? Look at the politics of 2008 – 2010. Voters trashed the party in power every chance they got. In 2008, they drove a wave election for Obama. Obama & Co. then felt their way through the worst of the post-bust economic crisis. They paid a huge political price. The loss of their Senate super-majority (when Scott Brown won Ted Kennedy’s seat in Massachusetts) and the “shellacking” that lost the House in 2010.

11 years later, we’re facing another massive crisis. Expect a similar “throw the bums out” response.

A Bonfire of the Incumbents

In general, this election is going to be “bonfire of the incumbents.” Possibly of both parties. But definitely the party in charge. Anyone who didn’t come into 2020 with a decent approval rating.

In the Senate, Republicans in Colorado, Iowa, Arizona, and Maine are all done. That’s enough to probably give the Senate to the Democrats. Note that Mitch McConnell also has a low approval rating back “home” in Kentucky (a place he only visits occasionally). He faced a credible challenger in Amy McGrath (donate here), but was rated a likely win a few weeks ago. Those polls and projections are now meaningless. The epidemiological charts suggest he’s gone.

In the House, anti-incumbency will probably cut both ways. So lets assume losses on both sides with a Trump-driven tilt against the Republicans. Pelosi stays in power.

Trump is probably toast. Absent a medical and economic miracle, there are too many on-camera mis-statements that will play in a continuous barrage of commercials. In a campaign that will pivot on Healthcare – a serious weakness for him. He can’t even hold rallies (more on that in a later post). And he probably starts lashing out more as the crisis wears on.

Biden’s primary qualification was always “not Trump” more than any particular affection. That worried me a month or so ago. But its probably the perfect message now. “I’m not that objectionable” will be good enough for a whole lot of people to just stay home or (maybe) vote against Trump.

Election 2020 is Now About Healthcare and Bailouts. Or Maybe Bailouts and Healthcare.

Looking ahead from here, the Democratic election messaging will pivot on two issues. Healthcare and “bailouts.” Or maybe “bailouts” and then Healthcare. It depends on how sleazy the next few months of stimulus end up looking.

I almost feel sympathy for the Republicans. They are in the same position Obama found himself in after 2008. Mitch McConnell wrote the playbook for “how to make political hay out of tough governing choices made by the other party.” Nancy and Chuck are following that playbook now.

Take today, where McConnell failed to advance the process in the Senate via a cloture vote blah blah blah. What does that really mean? He’s probably lost the initiative to Pelosi.The House can now pass a bill and send it to the Senate before McConnell can get his own bill passed. He either swallows the House template or he’s on the hook for “obstruction” if he tries to force through his own. Either way, Mnuchin is back to negotiating with Pelosi and she’s pretty good at the dark arts.

Also notice how the Democrats explained their objections – the supposed “slush fund” in the bill. They will make every vote about sleaze – real or imagined. Money to workers and SMB’s are popular. “Bailouts for big business” are not popular. So the party out of power naturally maximizes its support for the popular stuff and minimizes its support for the unpopular. Let the guy in power take out the garbage. Make sure McConnell and Trump own the “bailouts” that the economy (fairly) and their donors (much less fairly) demand.

Re-Branding “Stimulus” as a “Slush Fund”

Look at the politicking around the current stimulus package Stimulus package. Democrats have zeroed in on the $450bn “slush fund” for big company bailouts.

Republicans are trying to avoid disclosing who gets funds until after the election. Why? At least partly because a chunk is going to go to the Trump organization (code word “hospitality industry”). Which might, actually, be totally legit. But there’s no way the Dems are going to let that (or any other bailout) happen in the dark.

The Republicans argue (reasonably) that no company would take government money in 2008-2009 because it signaled higher default risk. There’s a certain irony to seeing them defend a reasonable (but untenable) position for once…

Its a useless fight anyway. Bailout news will leak anyway (especially a Trump bailout). And it will be all the worse politically for leaking.

In terms of the Democratic response, lets say the House passes the same bill as the Senate, but strips out the $450bn for “big business.” Leaving the (smaller?!?) $350bn for small business, the expanded unemployment benefits, and the checks to individuals. “We need to act now to help Main Street America! Wall Street can wait a week or two! A stand-alone own bill with careful protection of taxpayer money! No bailouts! No slush fund!” The speech practically writes itself.

McConnell could pass that House bill. But that would leaving him heavy lifting alone on a stand-alone big business bailout bill. Democrats will label that a “slush fund” no matter how well constructed it is.

Or McConnell spends the next few days/weeks “fighting to preserve the slush fund.” Sucks to be in charge…

We’ll see what happens. But, politically, every delay and mis-step today only helps the Democrats in November. They know that. So expect a lot more drama. And a lot more delay, disguised as a battle against sleaze.

Kelly Loeffler (R – GA) is Toast.

We can already count at least one senate Republican seat as lost. Kelly Loeffler was appointed to fill a vacated seat in 2020. So voters in only-now-pink Georgia don’t know much about her. By November, the ONLY thing they will know about her is her suspiciously well-timed stock sales in February – right after she got a secret Coronavirus briefing. Its probably too late for her to step aside and her Democratic opponent is a bona fide Congressman not a wingnut. Which means he probably takes her seat.

Posted inUncategorized|Comments Off on 2020 Election. Bonfire of the Incumbents. Pivoting on Healthcare and “Bailouts.” Georgia (R) Senate Seat Already Lost.

I’ve recently sold all my index funds and am holding on to only two stocks (more on those in a later post). The reason why experts (correctly) tell you NOT to do this is because people “never” buy back in. You miss the following upturn. Following that advice, I did not sell my index funds in 2008. A few years later, those losses really were just a blip. That is what most folks should do.

But I called the bottom in 2009 (really – see below). And I bought back in. So the lesson I took away was “WTF was I thinking? I knew it would be really bad!! And it wasn’t priced in. Retreat and live to fight another day you dipsh*t!” To that end, I have promised myself I’ll buy back in. Either 1). When all hope really looks lost. 2). In 3-6 months if it looks like I was wrong. If you sell out, you MUST do the same.

I Actually Did Call The 2009 Bottom. I May Not Manage That Again.

FWIW, I did actually call the bottom (in a note I can’t share) in March 2009. I was working at a large mutual fund complex and I wrote an internal note titled “My Centre is Yielding. My Right is Retreating. Situation Excellent. I Attack!” The title says it all.

Of course, the portfolio managers mostly ignored that note. Maybe they didn’t get the historical reference to battle of the Marne? More likely they were too busy hiding under their desks. Even more likely they didn’t take me all that seriously.

But I did put the one (big) chunk of deferred bonus cash I had back into the market. So I did pretty well out of it. I’d have done better if I’d sold my index funds a few months prior. So I’m doing that now.

There is ZERO guarantee I am right. Nor am I all that confident in this move. My need to preserve immediate capital is also probably different from yours. So do not take this as advice. But I thought I’d share the perspective.

First the Earthquake, then the Fires.

I think we are looking at a “double whammy” scenario similar to the 2008-2009 crisis. Or, if you like, the 1906 San Francisco earthquake. The initial shock (the earthquake) was really bad. The secondary shock (fires that burned what was left standing) was much much worse.

The Coronavirus is “the earthquake.”

The economic disaster from months of isolation are “the fires.”

1H 2008 was the Earthquake.

In the 2008 crisis, the initial shock was in the first half of the year. A whole bunch of mortgage-backed securities, Bear Stearns, and Countrywide Financial going bust. The market dropped about 17-%-18% from its highs, but it was all fairly orderly. “Everyone” (including myself) thought the authorities were reasonably on top of it. It was a bad crisis in a big corner of the financial markets, but still a contained crisis. We were all wrong.

2H2008-1H2009 Brought the Inferno.

It is easy to smear the 2008 crisis into one long memory of misery. But the real horrors started only after Lehman Brothers went bankrupt. Followed by the bailout parade of everyone else who would have gone bankrupt – AIG, General Motors, every bank under the sun, etc. etc. Followed by the Main Street damage of nationwide foreclosures (remember foreclosures peaked in 2009 and 2010). The “real” crisis hit one to two years later.

Have We Hit our “Lehman Moment?” I Don’t Think So.

Assuming the analogy is correct, are we in the “Bear Stearns” phase or the “post Lehman” phase? Everything I read and hear tells me we are still way too complacent. The deaths haven’t piled up (yet). People don’t have friends and family in ICU’s (yet). Bars and restaurants are (still) open in most places. People are still talking about “when” schools might re-open this year (they won’t). Or when their kids athletic leagues will re-start (ditto). That’s a whole lot of parentheses above.

So the full extent of the future economic damage remains hypothetical. Just like the foreclosures of 2009-2010 as seen from mid-2008. When it gets real, it will “get real.”

I think I’ve got an information advantage living where I do (Berkeley, CA). We’ve been on total lock-down since Monday. Grocery stores, hardware stores, and (thankfully for everyone’s sake) liquor stores/pot dispensaries. But everything else is shut down tight. The experience of that (and seeing the resulting evaporation of ANY business activity) has really clarified things for me. Although the cabin fever still hasn’t set in (yet) and the wave of small business failures to come is still a hypothetical.

As best as I can tell, most of the country is still “cutting back” vs going cold turkey. In a few weeks, most Americans will live my present experience when (not if) their towns lock down too. With most Red States lagging the Blue states. Because polls show our current partisan divide extends even to a virus that threatens all equally?!? It boggles the mind.

I also see the same complacency around the government policy response. I’ve been (happily) surprised at how fast the idea of sending out checks has gained traction. But I’m been dismayed at the hopefulness that mooted action has sparked. I remain skeptical that Washington will act with appropriate speed and scale (more below).

I Hope I’m Wrong. Some Counter-Arguments Considered Below.

“We’re more gun-shy of crisis after 2008 and have already discounted in a worse scenario.”

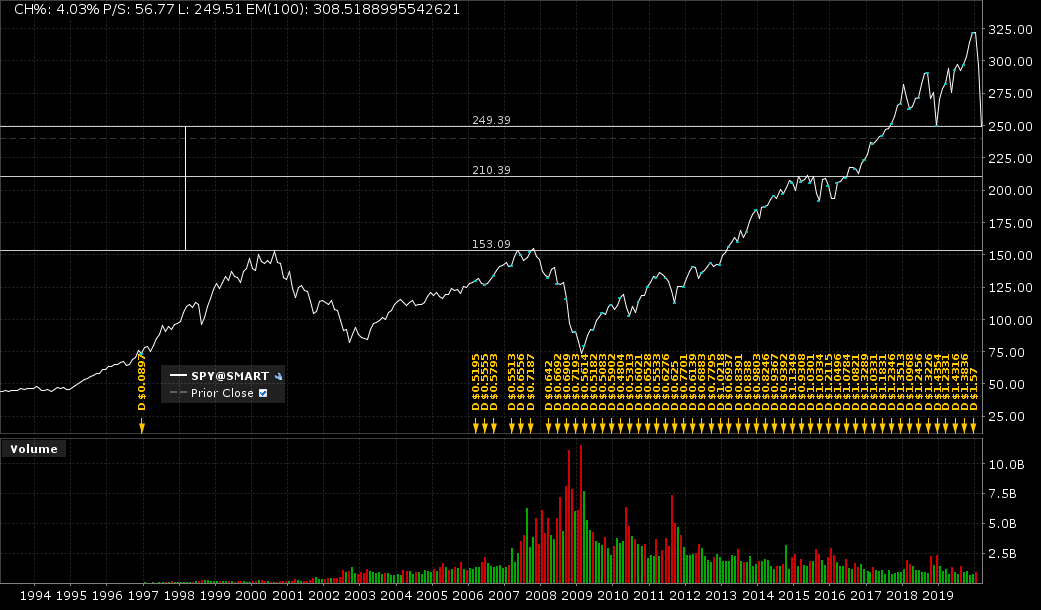

In market terms, we are already down @24% vs the 17% drop in 1H08. So maybe more bad news is priced in? Except that we “all know” a global pandemic that shuts down most non-essential business activity is going to be worse than a US-centric mortgage crisis. So it makes sense for the market to be down more in that initial drop.

Also we have only given back the gains from September 2017 so far. We could drop another 15% to the 2015-2016 plateau of S&P500 2,000. Or we could drop another 40% to 1,500 (the highs from 2008 and 2001). I’m just drawing arbitrary lines on a chart regardless (see below). In short, does the current S&P chart really fully reflect “months-long global economic shut-down?” I don’t think so.

The panic selling hasn’t hit yet. We are still seeing fairly orderly markets. I didn’t really notice the broader crisis 1-2 weeks ago (to my chagrin) because my own stocks were holding up well. I didn’t understand I happened to own “haven” stocks that people were buying when they dumped oil and cruise lines and etc… We’ve seen some hints of liquidation selling in the last few days. But we’ve also seen market rally attempts. People asking “when should I buy back in?” Also a whole lot of Americans haven’t dared peek at their brokerage and 401k statements yet. When they do, will they hang on? With the shops closed and the streets cleared, I don’t think so.

“Congress is Sending Out Checks and More Stimulus is Coming Etc. Etc.”

I already wrote a rant on this. I expect the governmental response will be inadequate and behind the curve. Until we see something approaching a “debt holiday” (no payments, no collections on mortgages, SMB debt, leases, corporate debt, credit cards, the whole kit and kaboodle), the government response probably isn’t there yet.

Checks are a good first step, but they will be swamped by the depth of the crisis. They need to be If that few thousand is a down payment on a much larger, longer, broader support package then maybe we avoid the worst of the hit.

Also like in 2008, a looming election will distract, distort, and delay US Governmental response. Note that the Democratic party has ZERO incentive to help Trump get re-elected. Their “smart” path (politically) is to look/sound concerned while throwing sand in the gears until November 4th. We all know Mitch McConnell would be moving like molasses if Obama were in office right now – deaths be damned. Mitch’s example blazed a path. Pelosi and Schumer may now follow. Craven self-dealing may end up the only bi-partisan thing left in Washington right now.

On the other side of that coin, don’t be surprised to see Fox News start up an increasingly shrill campaign to “postpone the November election because of the virus!!!” You read it here first 🙂

“The Financial System is More Resilient After 2008.“

Yes. No thanks those who’ve worked so hard to water down that legislation in the years since. But things are still in much better shape. If we were facing a mere 100 year flood, we’d probably be OK. But this argument doesn’t square with the economic reality of months-long global shut down. This is a 1,000 year flood. Rationally, no efficient financial system SHOULD be designed to handle that. So it won’t, Something will break.

Only when the tide goes out do you discover who’s been swimming naked. – Warren Buffett

Someone big out there is going to be caught swimming naked – holding too much debt with too little liquidity. And they will go bust. Which will cause other folks to go bust. Until we see that first wave of bankruptcies, we haven’t tested the system. The secondary wave of bankruptcies will start the real stress tests. The third and fourth waves will be the real tests. We haven’t seen the first bankruptcy yet.

We also haven’t seen the “little people liquidations” yet. The restaurant owner cashing out his portfolio to try and stay afloat. The middle class family that just bought the new house cashing out the 401k to make the mortgage and put food on the table. The debt-dependent wealthy families that lose a breadwinner or ran with too little cash cushion because “bad things only happen to poor people” (those same folks who had to sell their houses in tony suburbs during the mortgage crisis). All that is to come.

How I Called the Bottom in 2009. It Just Couldn’t Get Any Worse.

Lets be clear about the ONLY thing I knew writing that note back in March 2009. I had NO IDEA when it would get better. I just knew it couldn’t get (much) worse. The title says it all. “My Centre is Yielding. My Right is Retreating. Situation Excellent. I Attack!” Sometimes attacking is the only defense you have left.

We’d already been though months of liquidation in markets. All sellers, no buyers. That week, two of the networking equipment companies I covered told me customers were making capital plans on a rolling two week basis (vs a typical 1-3 years). In other words, the demand and planning horizon had shortened to hand-to-mouth, step-by-step. Abject fear.

That is what a bottom looked like back then. It might end up being what one looks like now. And we aren’t close to that yet. I hope I’m wrong.

Charts and Addendums.

* It took me a while to get my head wrapped around the scope of this crisis. In short, the stocks I owned were actually doing great. So the disaster befalling the broader markets over the last few weeks didn’t register as it should have. The only special pleading I’d make in my defense is that damn Saudi/Russia oil pumping war that came out of left field for most folks (including myself). Scary how that has been almost forgotten a week later.

* I hit this moment of clarity this Monday, March 16th. I’d talked to some friends were weren’t (yet) stuck at home by government order. By pure chance, I’d also watched a clip from the movie “Margin Call”(see below – do watch it). Actually watch the whole movie. It remains the most realistic Wall Street movie I know of – no villains no heroes just a brutally honesty-among-thieves, zero-sum game. For a reminder of how DC really works, I’d recommend the movie “Wag the Dog.”

* It is worth reading the background to Foch’s quote “My Centre is Yielding. My Right is Retreating. Situation Excellent. I Attack!” A link to the Wikipedia article. https://en.wikipedia.org/wiki/First_Battle_of_the_Marne