Looking ahead, we probably face either (mild) inflation or debt deflation.* Both leading to the same place. Losses on assets.

What we are watching right now is “the assets” twisting and squirming to try and find a way for someone else to take the pain. In more simple terms. Rich people (assets) trying to somehow shift the pain to poor people (labor market). Like we chose to do in 2008. Homeowners suffered most of the pain (paving the way for Trump’s takeover and the effective destruction of the “traditional Republican” party, but I digress).

Don’t think it is going to work this time around. Our current state is…

- …labor market looks fine. If you are in the bottom quartile, it looks awesome (see the “Wage Level” tab here, 4th quartile is “poor people.” 1st quartile is “rich people.” It explains a lot of the angst out there)

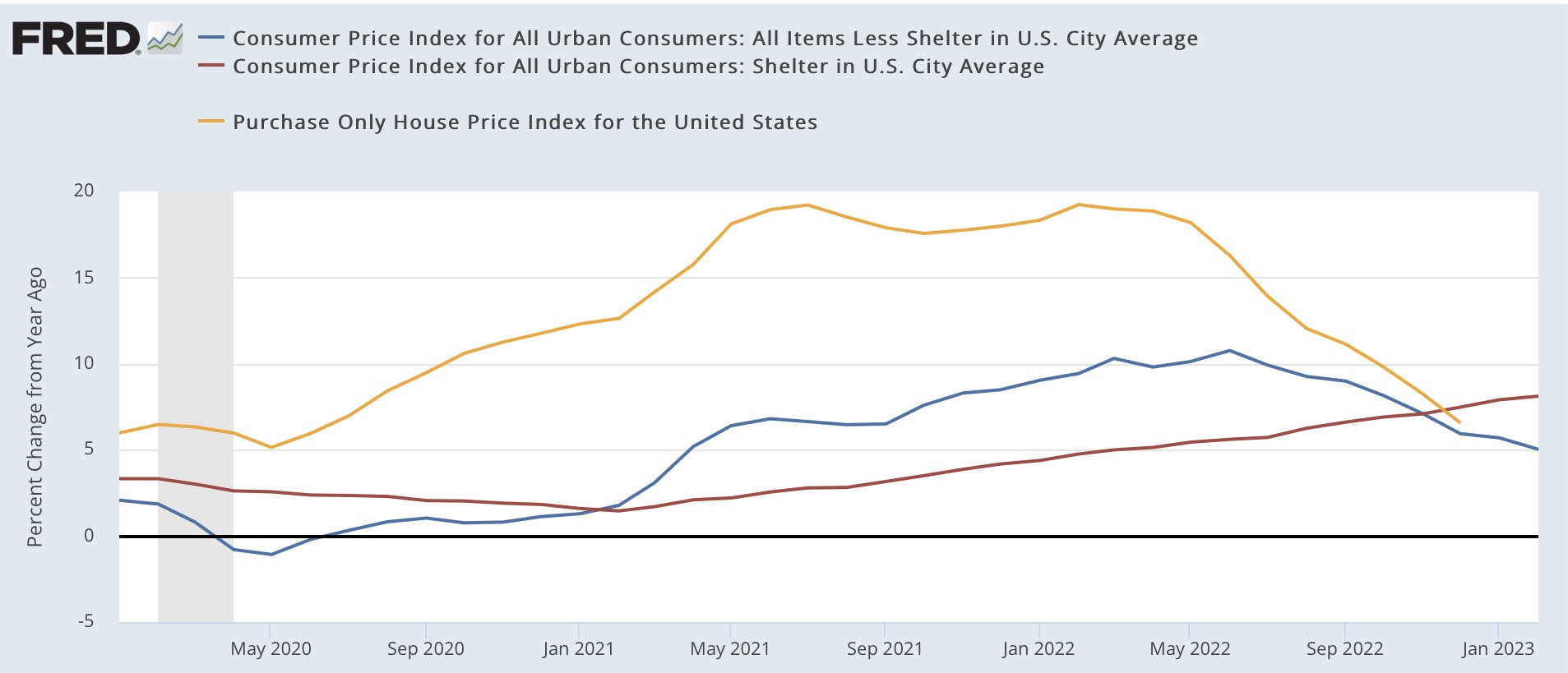

- …a LOT of assets are already carrying nasty mark-to-market losses. When rates go up, stuff priced in a lower rate past goes down…

Near-term future. The Fed either…

- …raises rates too high for too long. CRACK!. Another crisis and debt deflation. 2008 scenario.

- …raises a bit to save face, then starts cutting. HSSSSSSS….

- Inflation stays positive for a while (2% to 4% range?). Assets lose more value.

- Labor stays solid and wages keep creeping up for the bottom 1/4 (they have gotten HUGE gains in the last 2 years). Prices don’t keep up. Profits go down.

Is there a middle scenario? No mega-crisis, but assets don’t take a hit? Maybe? “The assets” are definitely searching for that easy exit.

- Maybe if we keep raising rates, maybe the labor market will finally break?!? The PR is “to slay inflation and protect the little man.” The un-spoken aim is as much to arrest continued wage gains and bargaining power. The problem? A labor market break would have to happen in the next few months. That doesn’t look likely. Especially as 4.5 points of rate increases haven’t done much so far (except wreck the banking system).

- If not, is there some other clever way we can socialize the losses and privatize the remaining profits? Like today’s plea by regional banks to insure 100% of deposits for 2 years. Note they are not also volunteering to submit to the more strict regulatory regime they wiggled out of a few years ago… A government guarantee to gamble for 2 years => “privatize the gains.” Why some Bank CEO’s are OK with a crisis.

Maybe “the assets” find a partial way out? I don’t see a way to socialize the losses (pushing the pain into the real economy) absent a major crisis like 2008. Maybe that is why some people seem OK risking another 2008? 2010-2020 was a pretty good decade for some…

But I’m not sure the Fed will play along this time around. The trail of blame here leads a little too obviously to the Fed’s doorstep. That (highly political) institution is already squirming to avoid taking the rap. So some near-term losses probably get socialized. The right thing to do to keep the banking system running. But the Fed isn’t likely to sacrifice itself to cut losses outside of its immediate reach. The best they can do is offer palliative care (ie. rate cuts).

Long-term future? Either…

- …a virtuous circle in the real economy. Higher wages flow through to more demand. Tight labor markets = higher productivity (robot waiters here we come).** Investment. Things really start humming. This is great for everyone EXCEPT the people suffering losses from 2%-4% inflation chewing up the 2008-2022 assets priced for a low-rate regime.

- …the air goes out of it. Like in post-2008, the virtuous circle never gets going because too much money leaks out in each turn of the cycle. Bled out of the real economy supply/demand cycle (really the wages/spending cycle). Leaking into “assets” piled on top of an increasingly stagnant real economy.

What is deeply annoying (to me) is that I was pretty much here in my thinking about 2 years ago. But I have managed the last 2 years pretty badly. I couldn’t/didn’t see through the logic of my own damn argument. Sigh….

** Productivity gains are the sole driver of economy-wide prosperity. The standard MBA myth is “far-sighted, profit seeking executives drive productivity gains.” Economic history suggests rising wages are a more powerful driver economy-wide productivity gains. Why? People are lazy. Managers are people. Without the goad of higher wages, they don’t look for productivity gains. But, when their backs are to a wall, they (like most people) get creative about finding a way out. The inverse of “Necessity is the mother of invention…” is “your average Joe doesn’t do much unless circumstances force them to…“